Section 100A: if you want BBlood, you’ve got it: 100A and capital amounts

On 19 September 2022, Justice Thawley of the Federal Court handed down his decision in BBlood Enterprises Pty Ltd v FCT [2022] FCA 1112 (BBlood), the most recent decision on section 100A of the Income Tax Assessment Act 1936. The Australian Taxation Office (ATO) was successful in arguing that section 100A applied.

BBlood follows the Full Federal Court appeal, decision still to be handed down, of the decision of Logan J against the ATO in the section 100A case of Guardian AIT that we wrote about here. The ATO appealed the decision of Logan J with the Full Federal Court hearing the appeal in October 2022. The decision is expected later this year.

Thawley J also held in BBlood that:

the facts amounted to dividend stripping within the meaning of section 207-155 of the Income Tax Assessment Act 1997; and

an assessment could not be made until a notice of assessment with the taxable income and tax payable was served on the taxpayer. The uploading of the information on the portal, which the taxpayer accessed, did not constitute serving of the notice.

This article focuses on the section 100A elements of BBlood.

What was BBlood about?

BBlood involved a share buyback and the differences between trust and taxation concepts of income. BBlood has factual similarities to Example 8 of Draft Taxation Ruling TR 2022/D1 and Example 10 of Draft Practical Compliance Guideline PCG 2022/D1 issued by the ATO in February. The ATO considered this a ‘red zone’ arrangement.

The facts in BBlood can be summarised as:

In the 2014 income year, a company with retained earnings (IP Co) bought back shares held in it by a discretionary trust (IP Trust).

The proceeds of the buy-back (about $10 million) paid by IP Co to IP Trust were deemed to be a dividend for tax law purposes. However, the share buy-back dividend constituted corpus of the trust for trust law purposes.

The deemed dividend was fully franked. Although it had never received income, the IP Trust also received income in the 2014 year of about $300,000. A newly introduced corporate beneficiary (BE Co) was made presently entitled to the trust income of $300,000.

The consequence of BE Co being presently entitled to the trust income was that it was assessed on the trust’s net (tax) income of $10.3 million, which included the share buy-back dividend. The tax payable by BE Co in relation to the share buy-back dividend was offset by the franking credits attached to the deemed dividend.

Thawley J held that section 100A applied to deem BE Co not presently entitled to the trust income and IP Trust was assessed on the net income under section 99A.

In the 2014 year, a further six private groups that were clients of the same advisor implemented similar arrangements to that in BBlood. One of those groups settled before the BBlood hearing and the proceedings relating to the other five groups were stayed pending the outcome of BBlood.

BBlood and Guardian AIT compared

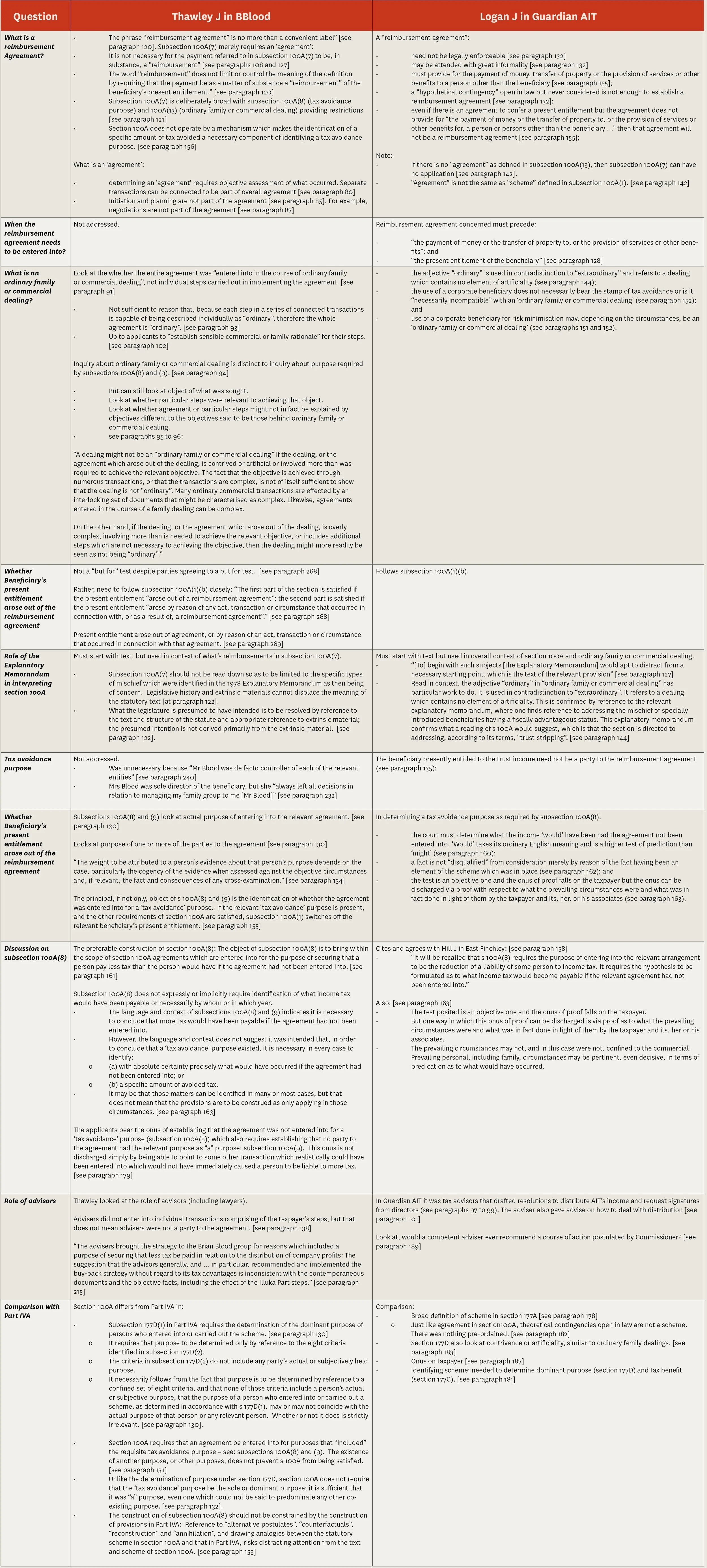

At the date of writing, we do not know if the taxpayer will appeal the decision of Thawley J in BBlood. The ATO appealed the Logan J decision in Guardian AIT and that appeal has been heard (decision pending). The table below looks at what Thawley J and Logan J said on various aspects of section 100A. However, care should be exercised in drawing broad conclusions as the comments were in the context of the facts of the specific cases.

What does BBlood mean?

At the date of writing whether the taxpayer will appeal the decision in BBlood is unknown. However, BBlood raised interesting points about the scope of section 100A:

the payment required under section 100A was the actual buyback payment from IP Co rather than a payment going somewhere else;

while section 100A refers to “presently entitled to a share of the income of the trust estate”, due to differences between trust income and net (tax) income, BBlood applied to an amount that was capital under trust law concepts of income; and

(related to the previous point), that the beneficiary received the benefit of the present entitlement to the income, the reimbursement agreement arose out of the capital, is not a defence to section 100A applying.

This last point is important as there has been commentary, including by the ATO, that if the beneficiary is paid the amount of the present entitlement to income, section 100A does not apply. BBlood suggests in certain circumstances that is not the case.

Further, while Thawley J says ordinary family or commercial dealings can be “complex”, the statement that, “[o]n the other hand, if the dealing, or the agreement which arose out of the dealing, is overly complex, involving more than is needed to achieve the relevant objective, or includes additional steps which are not necessary to achieving the objective, then the dealing might more readily be seen as not being “ordinary”” should serve as a warning to advisors when tax planning.

As we have written before, 2022 has shaped as the “Year of 100A” for taxpayers and their advisors in the SME and private wealth market. The judgment in BBlood adds to the jurisprudence on section 100A and is welcomed given the awkward drafting of section 100A, and the obscure nature of the ‘ordinary family or commercial dealing’ exception. However, this is not the end with the next instalment likely to be the Full Federal Court handing down its decision in Guardian AIT or the ATO finalising its views on the application of section 100A (which it has said should be before the end of 2022).

Watch this space!

(Honourable mention to AC / DC for the name of this article)

For more information please contact:

Neil Brydges

Principal Lawyer | Accredited Specialist in Tax Law

M +61 407 821 157 | T +61 3 9611 0176

E: nbrydges@sladen.com.au

Daniel Smedley

Principal | Accredited Specialist in Tax Law

M +61 411 319 327 | T +61 3 9611 0105

E: dsmedley@sladen.com.au

Rob Warnock

Principal Lawyer

T +61 3 9611 0155 | M +61 419 892 115

E: rwarnock@sladen.com.au

Edward Hennebry

Senior Associate

T +61 3 9611 0113 | M +61 405 847 261

E: ehennebry@sladen.com.au

Laura Spencer

Senior Associate

M 0436 436 718 | T +61 3 9611 0110

E: lspencer@sladen.com.au