AusNet v FCT and back-to-back rollovers: nothing else matters?

AusNet Services Limited (AusNet) applying for special leave to appeal to the High Court from the decision of the Full Federal Court in AusNet Services Limited v FCT [2025] FCAFC 21 (AusNet FFC), but seemingly not on the ‘nothing else’ aspects, raises the question of what the case may mean for the proposed guidance by the Australian Taxation Office (ATO) on ‘back-to-back CGT rollovers’.

More specifically, a feature of the AusNet litigation was whether the last in a series of three scrip-for-scrip exchanges satisfied the “nothing else” requirement for rollover under Division 615 of the Income Tax Assessment Act 1997 (1997 Act). The judges said ‘yes’. The ATO, since 2018, has said that it intends putting out guidance on “sequential transactions and the 'nothing else' condition of a rollover.”

This article does not discuss other aspects, such as the ratio requirements in section 615-20 of the 1997 Act, of the AusNet litigation.

Background - AusNet

In AusNet FFC, the Full Federal Court, by majority, upheld the decision by Hespe J in AusNet Services Limited v FCT [2024] FCA 90 (AusNet FC) that Division 615 rollover applied to a scheme of arrangement by AusNet during the year ended 30 June 2015.

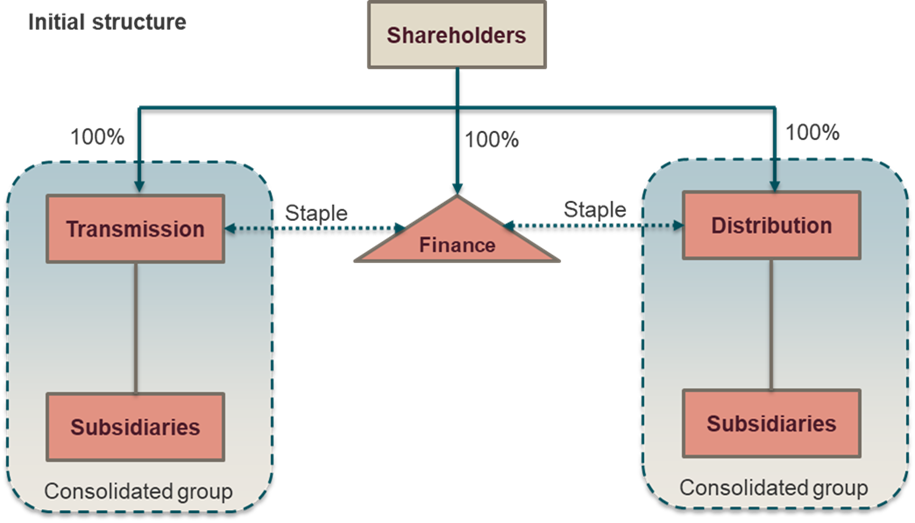

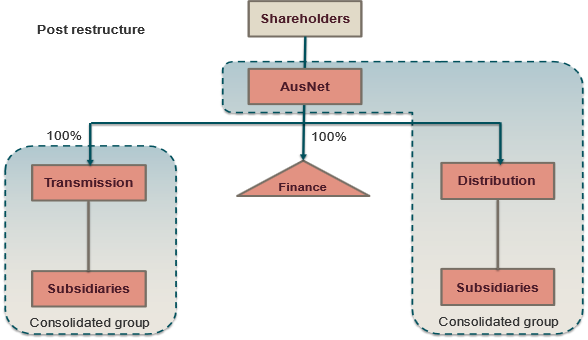

The AusNet group was a triple-stapled structure, made up of two companies, AusNet Services (Transmission) Limited (Transmission) and AusNet Services (Distribution) Limited (Distribution), both with their own consolidated groups, and a trust, AusNet Services Finance Trust (Finance).

On 18 June 2015, the AusNet group decided to un-staple and rollover each of the entities into a shelf company, AusNet, which would become the new head company of the (former) Distribution consolidated group. After the three companies were unstapled, AusNet acquired each of the three entities under scrip-for-scrip exchanges in the following order, Transmission, then Finance, then Distribution. The pre-and-post structures of the AusNet group are below.

On 1 July 2015, the Commissioner issued Class Ruling CR 2015/45 saying that Division 615 rollover relief would apply to the restructure under Division 615. However, AusNet objected to income tax assessments issued to it on the basis that Division 615 did not apply to the scheme of arrangement by which it came to be the holder of shares in Distribution.[1] This would entitle AusNet to an uplift in the cost bases of assets formerly held by the Distribution income tax consolidated group.

The Commissioner denied the objections and AusNet appealed to the Federal Court saying that the requirements of paragraph 615-5(1)(c) of the 1997 Act could not be satisfied. [2]

More specifically, AusNet argued the requirement under paragraph 615-5(1)(c) that the Distribution shareholders, under a “scheme for reorganising its affairs”, disposed of all their Distribution shares to AusNet in exchange for shares in AusNet and “nothing else” was not satisfied. AusNet argued that the shareholders received something else in the form of a “boost” in the value of their existing shares in AusNet.

Hespe J in AusNet FC dismissed this argument saying (bold added):

“As a matter of statutory interpretation, the requirement in s 615-5(1)(c) is that under a scheme for reorganising the affairs of Distribution, the exchanging members (being the existing owners of the shares in Distribution) dispose of their shares in Distribution “in exchange for” shares in the applicant “and nothing else”. By its terms, s 615-5(1)(c) focusses on that which a shareholder receives under the scheme in exchange for the shares. It does not look to the consequences of the scheme, but rather the consideration or quid pro quo received for the disposal of the shares.

…

Under the terms of the Distribution scheme of arrangement, the Distribution shareholders received one share in the applicant in exchange for the disposal of each Distribution share and “nothing else””.

AusNet appealed to the Full Federal Court which, by majority, in AusNet FFC dismissed the appeal. However, on the “nothing else” requirement, all three judges dismissed AusNet’s arguments:

Logan J (bold added)

“Considered as an abstract proposition, divorced from reading the text of s 615-5(1)(c) in context, there is much to recommend the appellant’s submission. However, read in context, the focus of this provision is just on the consideration for the exchange. The intention of the parenthetical qualification “and nothing else” is to confine the application of this criterion just to an exchange where shares in the interposed company, as opposed to additional consideration, are received. It does not look to incidental consequences of the “exchange”. Adopting that construction is congruent with the notion of the reorganisation, already discussed, for which s 615-5(1)(c) provides and with s 615-1, “in exchange, you become the owner of new shares in another company”. It is also congruent with the heading of s 615-5, “Disposing of interests in one entity for shares in a company”. I do not therefore accept the construction of s 615-5(1)(c) pressed for the appellant.”

Thawley J (bold added)

“First, for the reasons given by Kennett J, the “and nothing else” requirement in s 615‑5(1)(c) is directed to the contractual consideration received by a shareholder in exchange for the shares, not an inquiry into whether the exchange resulted in the shareholder receiving a “boost” in value.”

Kennett J (bold added)

“The first issue that requires attention is whether any “boost” to the value of shares that the Distribution shareholders already held in Ausnet is relevant to the scheme satisfying the requirements of s 615-5(1)(c). The provision, it will be recalled, refers to a disposal of shares “in exchange for shares in the interposed company (and nothing else)”. The critical integer, therefore, is what the shareholder receives “in exchange” for their shares or units in the original entity. That language directs attention to consideration in the traditional contractual sense: it is concerned with what tangible benefits pass from the acquirer of the shares or units (the interposed company) to the person disposing of those shares or units. It does not invite a more general inquiry into the consequences of the transaction. The primary judge recognised this (at [103]) and it formed part of her Honour’s reasons for rejecting Ausnet’s submissions.

This understanding is supported by the legislative history. …”

That is, in both AusNet FC and AusNet FFC the courts said that the “nothing else” requirement looks to what is received in exchange for the shares – the quid pro quo per Hespe J in AusNet FC – not the consequences of the scheme.

Proposed ATO guidance on back-to-back CGT rollovers.

The ATO has said since November 2018 that it will develop guidance on “sequential transactions and the 'nothing else' condition of a rollover” (Proposed Guidance). The ATO website currently states:

“This guidance will provide the Commissioner’s view on the use of rollovers for certain arrangements which may include the interpretation and application of the ‘nothing else’ condition in CGT rollovers.

The ATO is currently looking at arrangements where rollovers are used, including arrangements where rollovers are used in conjunction with another rollover or other transactions, and the public advice and guidance that would be appropriate to provide clarity to the ATO's position on these arrangements. This includes rollovers that have a ‘nothing else’ requirement”.

Rollovers that include a “nothing else” requirement include:[3]

Division 125 of the 1997 Act (demerger relief): “a new interest and nothing else”

Division 615 (rollovers for business restructures): “shares in the interposed company (and nothing else)”

Division 122-A and Division 122-B of the 1997 Act do not have a “nothing else” condition but include the conceptually similar requirement that consideration “must be only shares”.

Unlike scrip-for-scrip rollover under Subdivision 124-M of the 1997 Act, which does not have a “nothing else” condition, but allows for a partial rollover to the extent of ineligible consideration, for the rollovers with “nothing else” conditions, a breach of that condition means the rollover is not available at all.

The ATO website previously included the following with respect to the Proposed Guidance.

“Paragraphs 2, 3 and 55, and Examples 3 and 4 of Taxation Determination TD 2020/6 Income tax: what is a 'restructuring' for the purposes of subsection 125-70(1) of the Income Tax Assessment Act 1997? discuss aspects of sequential transactions.”

Paragraphs 2, 3, and 55 of TD 2020/6 do not refer to the “nothing else” condition but paragraph 7 does (bold added):

“If a step or transaction forms part of the restructuring of the demerger group, the particular step or transaction may affect whether or not the conditions to qualify as a demerger in subsection 125-70(1) (which include, through paragraph 125-70(1)(h), the requirements of subsection 125-70(2)) can be satisfied. Since under paragraph 125-70(1)(a) a demerger happens if there is a restructuring, the scope of the restructuring (including when it begins and ends) is also relevant to the 'nothing else' condition in paragraph 125-70(1)(c) (which examines what the owners of the original interests in the head entity may acquire under the restructuring) and the proportionate ownership test and proportionate market value test in subsection 125-70(2).”

Paragraph 55, while not referring to “nothing else”, summarises the ATO approach in TD 2020/6 (bold added):

“Accordingly, an interpretation of restructuring should be favoured which allows a proper evaluation of whether the specific conditions in Division 125 have been satisfied, and therefore whether or not the restructuring itself brings about a change in the economic position of original owners. This suggests that not only the delivery of the ownership interests referred to in paragraphs 125-70(1)(b) and (c) should be considered, but also any other previous or subsequent events, acts or transactions in a sequence of events, or acts or transactions sufficiently connected with those prescribed statutory steps to form part of a single plan. Commercial understanding and the objectively inferred plan for reorganisation determines which steps or transactions form part of the 'restructuring' of the demerger group”.

In TD 2020/6, the ATO view is that a series of distinct steps and transactions, even if those transactions are legally independent, can form a single arrangement, plan, or reorganisation. Including or excluding steps in the restructuring may cause the demerger to not satisfy the “nothing else” requirement in the demerger provisions.

With respect to back-to-back rollovers or sequential transactions including rollovers, the question is therefore - if the subsequent rollover (or transaction) is treated as part of the same transaction would the taxpayer be receiving something else and thus fail the requirements for rollover relief? The ATO view, when considering TD 2020/6, may be ‘yes’.

What does AusNet mean for the Proposed Guidance?

Will the view of the courts in AusNet that the “nothing else” requirement looks to what is received in exchange for the shares – the quid pro quo per Hespe J – not the consequences of the scheme, influence the Proposed Guidance? Or will the Proposed Guidance have views like those in TD 2020/6?

While AusNet FFC is, on the “nothing else” requirement, a unanimous decision, and the ATO must not administer “the statute in a manner contrary to the meaning and content as declared by the Court”, [4] the Proposed Guidance is likely to be broader than the specific issue considered in AusNet. Further, the statutory context of “nothing else” in the other rollovers is different to that in Division 615 and Subdivisions 122-A and 122-B refer to “must be only” rather than “nothing else”.

Nonetheless, one would like to think that four Federal Court judges, in separate judgments, coming to the same interpretation of “nothing else” should be, at a minimum, highly influential on the ATO views in the Proposed Guidance.

While we may like to think that, in the end, the Proposed Guidance could be like the words of Metallica in the song ‘Nothing else matters’:

Never cared for what they do

Never cared for what they know

But I know

For more information please contact:

Neil Brydges

Principal | Accredited Specialist in Tax Law

M +61 407 821 157 | T +61 3 9611 0176

E nbrydges@sladen.com.au

Daniel Smedley

Principal | Accredited Specialist in Tax Law

M +61 411 319 327 | T +61 3 9611 0105

E dsmedley@sladen.com.au

Kaitilin Lowdon

Principal Lawyer

M +61 402 859 214 | T+61 3 9611 0120

E klowdon@sladen.com.au

[2] This article does not discuss AusNet’s argument that the Distribution transaction did not satisfy the ratio requirements in section 615-20.

[3] The less common rollovers under Division 124-E, Division 124-F, Division 124-I, and Division 124-Q also include a “nothing else” condition.

[4] FCT v Indooroopilly Children Services (Qld) Pty Ltd [2007] FCAFC 16.