Sladen Snippet – New Div 296 tax – what we know and what we don’t?

By a media release dated 13 October 2025, the Treasurer confirmed that the former Division 296 Bill will not be reintroduced in the same form as the draft legislation introduced by Parliament in November 2023.

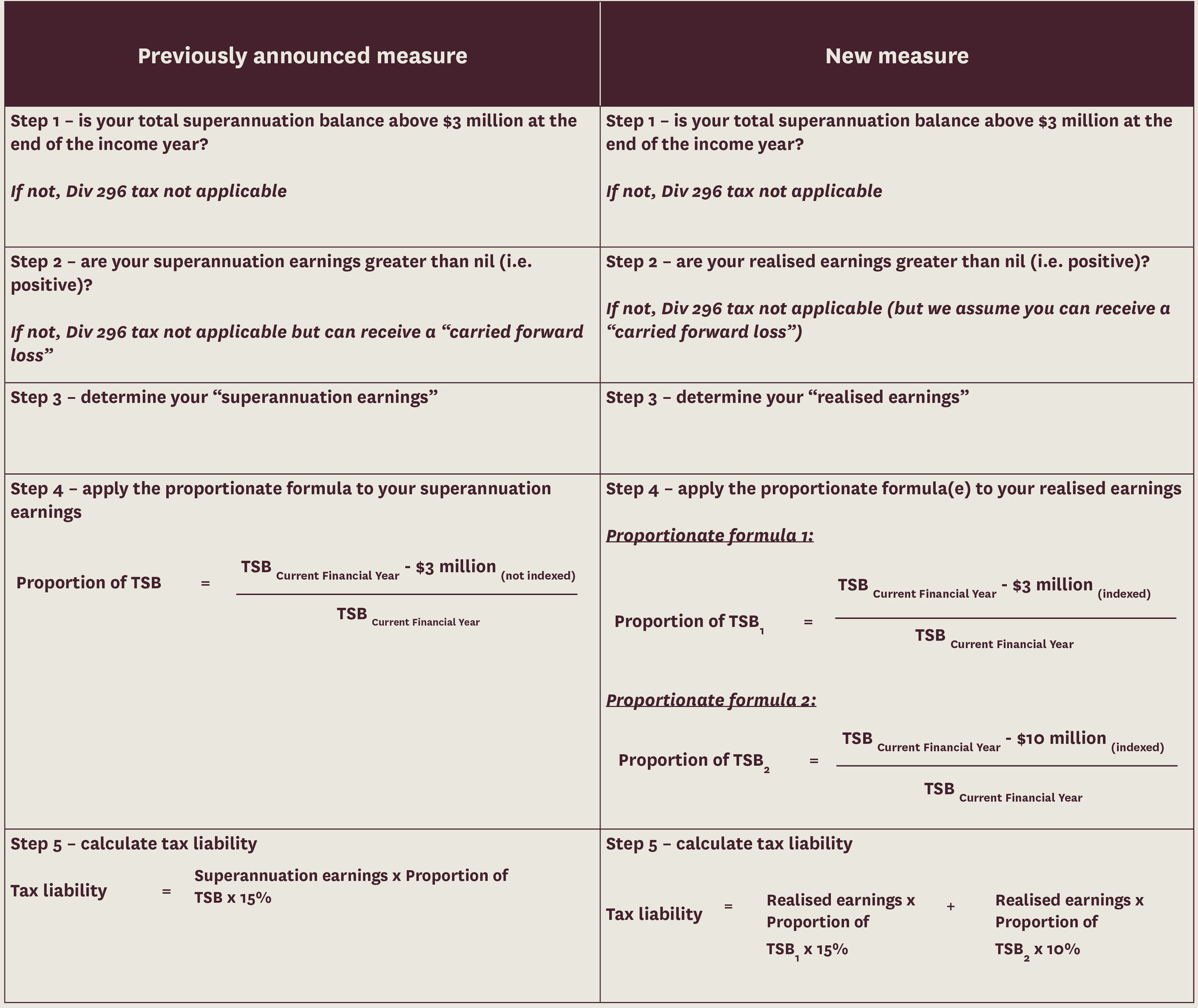

As discussed here, the Treasurer confirmed that key changes of the new measure will include:

instead of one unindexed threshold of super balances of $3 million, there will be two thresholds, both of which will be indexed:

$3 million (indexed).

$10 million (indexed).

For both thresholds, the Div 296 tax will apply to income and realised earnings, at a rate of up to 30% (earnings on balances between $3 million and $10 million) and up to 40% (earnings on balances over $10 million) – ie it will no longer apply to unrealised gains.

Start date pushed back to 1 July 2026 (from 1 July 2025).

What we know

The Treasury has released a fact sheet (Fact Sheet) outlining some of the mechanics of the revised measure. The table below compares the key features of the previously announced measure with those of the new measure, as described in the information sheet.

What are realised earnings?

The Fact Sheet does not definitively set out how “realised earnings” (also referred to in the Fact Sheet as “total earnings”) will be calculated. However, it provides the following comments:

Fund’s realised earnings will be based on its taxable income, adjusted for elements such as contributions and pension phase income. Calculations closely aligned to existing tax concepts.

In-scope members will then be attributed an appropriate share of the fund’s realised earnings based on existing reporting mechanisms or on a fair and reasonable basis. This would be supported by guidance from the ATO.

The ATO will then contact a super fund for the proportion of the fund’s applicable realised earnings for any individual with a TSB above the legislated threshold.

Funds undertake calculation of earnings and the share attributable to in-scope individuals and provide this information back to the ATO.

So, at this stage, we can guess that realised earnings may not have an exhaustive statutory definition but rather will rely on ATO guidance (eg in an ATO ruling, PCG and/or PSLA).

It also appears that it will be a calculation that will need to be made by the super fund trustee after a written notice is provided to that trustee from the ATO.

What we don’t know about realised earnings

Critically, what we don’t know, at this stage, in relation to the calculation of realised earnings is:

whether gains attributable to the period pre-1 July 2026 will be excluded;

assuming they are excluded, how super fund trustees will apportion pre and post gains;

whether public offer super funds will want to, or be able, to make these calculations across its membership base; and

how this calculation is to be made to these pre-gains that are in entities that a super fund is invested in – for example, companies and unit trusts.

The last point is of particular concern. For example, this would include where a super fund receives a distribution from a unit trust, or a dividend from a company, post 1 July 2026 that includes realised gains from assets held by that company or unit trust before 1 July 2026. If the unit trust or company is a related entity, the super fund trustee will likely be able to calculate the pre-1 July 2026 realised gains contained in the distribution/dividend but will the legislation or ATO permit that to be excluded from realised earnings.

For unrelated companies and trusts it is unlikely that the fund trustee will have the information to calculate the pre-1 July 2026 gains meaning they will pay Div 296 tax on these indirect pre-1July 2026 gains.

If these pre-1 July 2026 gains are not excluded from realised earnings, we can foresee that many super fund trustees will seek to dispose of assets or unwind company or trust investments as a result of the measure.

What else don’t we know

We also don’t know:

how much of the other provisions from the former Div 296 tax legislation will be retained;

whether, in light of the “40%” tax rate on $10 million plus member balances, members who have not otherwise met a condition of release will be able to withdraw their benefits above $10 million; and

how the measure will work for defined benefit pensions.

In the meantime, we wait and see

According to the Fact Sheet, the Government will implement the new Division 296 legislation “as soon as possible in 2026”.

Therefore, in the meantime, we wait and see.

Phil Broderick

Principal

T +61 3 9611 0163 l M +61 419 512 801

E pbroderick@sladen.com.au

Philippa Briglia

Special Counsel

T +61 3 9611 0174 | M +61 449 404 801

E: pbriglia@sladen.com.au

Jan Harnischmacher

Associate

T +61 3 9611 0158

E joh@sladen.com.au

Andrea Lin

Lawyer

T +61 3 9611 0189

E alin@sladen.com.au