Allocation of professional firm profits – the ATO moves the goalposts!

On 1 March 2021, the Australian Taxation Office (ATO) released Draft Practical Compliance Guideline PCG 2021/D2 Allocation of professional firm profits – ATO compliance approach (Draft PCG) that sets out the ATO’s proposed compliance approach to the allocation of profits by professional firms.

The Draft PCG is a fundamental change from the former guidance that the ATO suspended in December 2017. In effect, the Draft PCG puts most previously acceptable arrangements into the moderate or high-risk category. The Draft PCG does not explain the reasons or necessity for this shift.

How did we get here?

By way of recap, in 2015 the ATO released a document titled “Assessing the risk: allocation of profits within professional firms” (Guidelines) that contained three bright line tests (“Benchmarks”) whereby ‘individual professional practitioners’ (IPPs) were regarded as being of “low risk” of compliance activity if the IPP passed one of the following three Benchmarks:

Benchmark 1: ‘appropriate remuneration’: the IPP needed to receive remuneration benchmarked with reference to the lowest paid member of the upper quartile of the firm s/he works for;

Benchmark 2: ‘50% entitlement’: 50% or more of the income from the firm to which the IPP and their associated entities are collectively entitled (whether directly or indirectly through interposed entities) in the relevant year is assessable in the hands of the IPP;

Benchmark 3: ‘30% effective tax rate’: the effective tax rate must be 30% or higher on both income from the firm to which the IPP is entitled and income from the firm to which the IPP and their associated entities are collectively entitled.

On 14 December 2017, the ATO abruptly suspended the Guidelines as the ATO considered some taxpayers and/or advisors were misinterpreting and applying the Guidelines beyond their scope. The ATO said it would develop a replacement product in consultation with professional bodies and ad hoc consultation occurred from April 2018.

Following the suspension of the Guidelines, the ATO annually said that IPPs who entered arrangements prior to 14 December 2017 could continue to rely on the suspended Guidelines. For IPPs entering arrangements after 14 December 2017, the ATO recommended engaging with it.

What approach does the Draft PCG take?

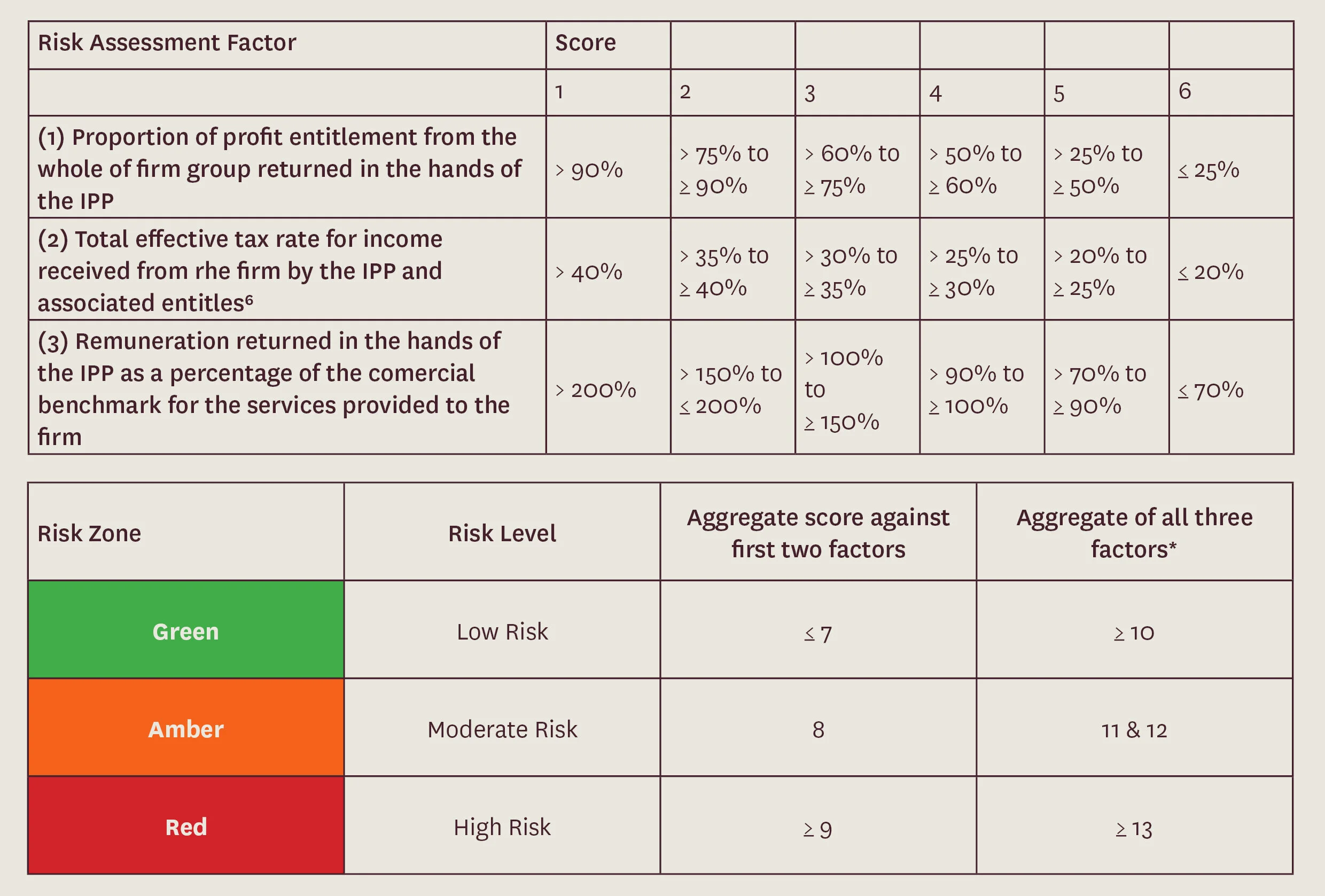

There are (some) similarities between the Draft PCG and the Guidelines, but considerable differences. The similarities are that there are three similarly formulated Benchmarks that look to:

Benchmark 1: the proportion of profit returned personally in the hands of the IPP to the total amount of income to which the IPP and his or her associated entities are collectively entitled;

Benchmark 2: the total effective tax rate paid by the IPP and their associated entities; and

Benchmark 3: the IPP should receive assessable income from the firm in their own hands which reflects an appropriate return for the services they supply the firm.

However, there are two key differences between the Draft PCG and the Guidelines:

1. to apply the benchmarks, two ‘Gateways’ must first be passed:

a. Gateway 1: the ATO expects there to be sound commercial rationale for entering into or using the arrangement or structure; and

b. Gateway 2: there must not be certain ‘high-risk’ features.

2. where an IPP's circumstances pass the Gateways, the IPP can apply the Benchmarks to receive a ‘traffic light’ risk assessment rating of green (low risk), amber (moderate risk), or red (high risk). If the IPP does not satisfy the Gateways, the risk assessment framework (below) is not available to the IPP.

Unlike in the Guidelines where the IPP needed to only satisfy one Benchmark, the Draft PCG requires an IPP that passes the two Gateways to apply both Benchmarks 1 and 2 with Benchmark 3 being optional to determine a risk rating.

An IPP with an effective tax rate of 30% returning 50% in their own hands would have satisfied two of the Benchmarks in the Guidelines (the IPP only needed to satisfy one). Under the Draft PCG, assuming the IPP satisfies the two Gateways, the IPP will receive a ‘score’ of ‘9’ classifying the IPP as ‘high-risk’.

The Draft PCG says “[i]f your arrangement does not have a low (that is, green zone) risk rating, we consider your arrangement, or your treatment of that arrangement, is at risk of giving rise to an inappropriate tax outcome. Therefore, we will generally conduct some form of compliance activity to further test the tax outcomes of your arrangement.”

Under the Draft PCG IPPs are expected to annually assess eligibility and document that assessment of eligibility.

The ATO moves the goalposts

There is a fundamental shift from the Guidelines. In effect, the Draft PCG puts most previously acceptable arrangements into the amber or red risk category. The Draft PCG does not explain the reasons or necessity for this shift.

Further, it seems counterintuitive for an arrangement that is commercially driven and does not exhibit high risk features – the Gateways are satisfied – to then be classified under the assessment framework as moderate risk (amber) or high risk (red).

Another key change is that one of the key tenets of the Guidelines was that they were structurally agnostic, that is they avoided the need for the ATO to get caught up in questions of structures and leading to different outcomes based on structures not economic consequences. The Draft PCG considers multiple classes of shares or units as a high-risk factor under Gateway 2 which introduces a bias towards certain structures.

Finally, by pushing most existing acceptable arrangements into the amber or red zone, and by introducing the necessity to self-assess annually, there is a significant compliance burden placed on IPPs.

The way forward

When finalised, the Draft PCG is to apply from 1 July 2021. ‘Commercially driven’ arrangements with no high-risk features entered before 14 December 2017 can rely on the Guidelines until 30 June 2021.

Transitional arrangements apply for IPPs whose arrangements were low-risk under the suspended guidelines but are moderate or high-risk under the draft PCG.

Submissions on the Draft PCG are due by 26 March 2021.

If you would like to discuss the Draft PCG, please contact one of our team members:

Neil Brydges

Principal Lawyer | Accredited Specialist in Tax Law

M +61 407 821 157 | T +61 3 9611 0176

E nbrydges@sladen.com.au

Daniel Smedley

Principal | Accredited Specialist in Tax Law

M +61 411 319 327| T +61 3 9611 0105

E: dsmedley@sladen.com.au

Rob Warnock

Principal Lawyer

M +61 419 892 115 | T +61 3 9611 0155

E: rwarnock@sladen.com.au

Rob Jeremiah

Principal l Accredited Specialist in Tax and Business Law

M +61 418 500 363 l T +61 3 9611 0103

E rjeremiah@sladen.com.au