The Payroll Tax Clampdown Against the Healthcare Industry Continues: the Optical Superstore Case

The Victorian Supreme Court’s decision in favour of the taxpayer has been overturned by the Victorian Court of Appeal. We have previously discussed the Victorian Supreme Court decision.

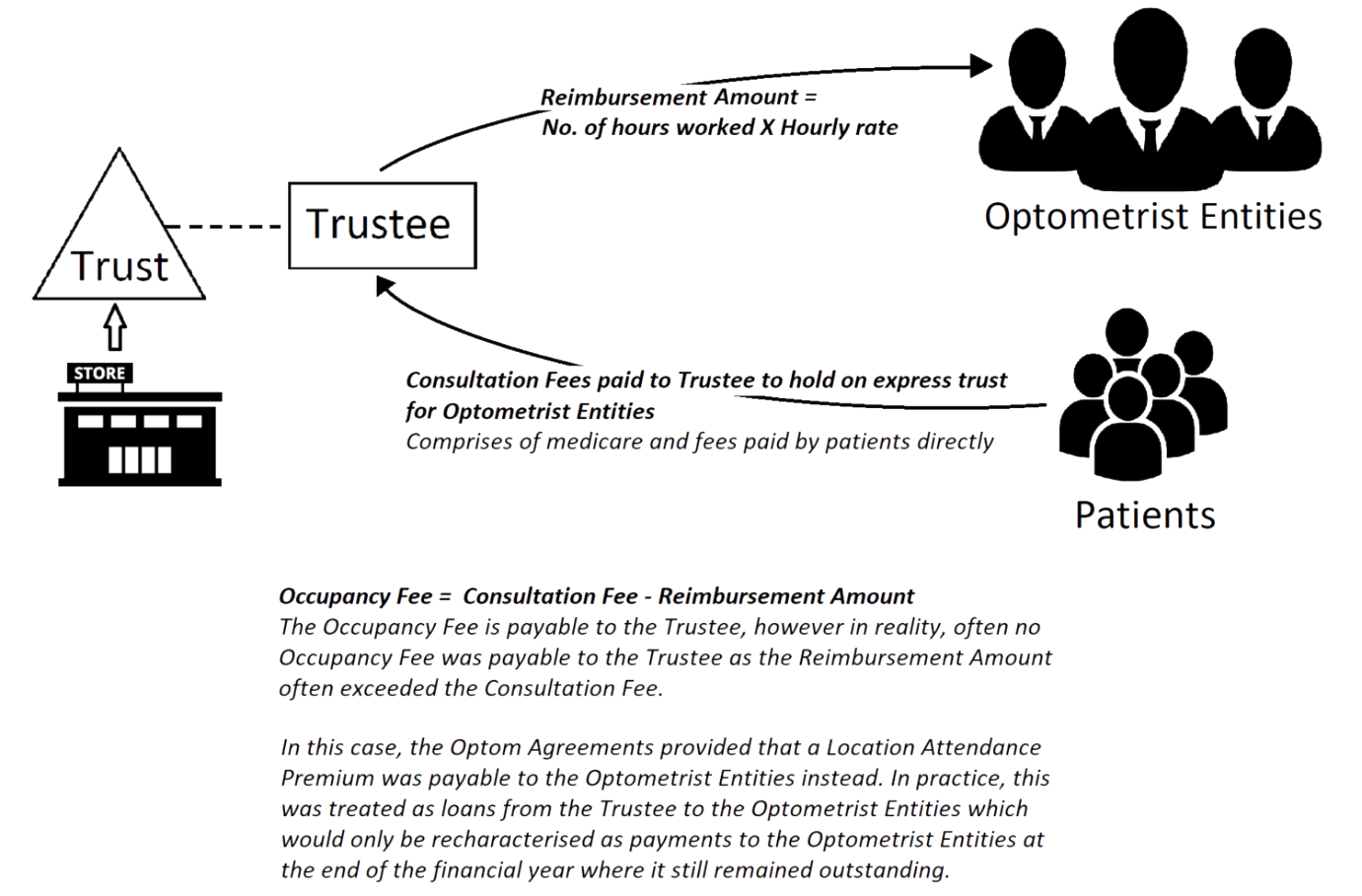

Summary of the facts

The matter involved the Optical Superstore Pty Ltd, a trustee of four related trusts which together carried on an optical dispensary business known as the ‘Optical Superstore’. There were Optum Agreements entered into with the Optometrist Entities (either directly with optometrists or with their respective companies or trusts) which entailed an arrangement under which the Optometrist Entities would operate in Optical Superstore locations. The arrangement included, in simple terms, the following payments:

The core question of the case is whether payments from the Trustee to Optometrist Entities should be taken to be wages under a relevant contract under section 35 of the Payroll Tax Act 2007. This section relevantly provides “amounts paid or payable by an employer during a financial year for or in relation to the performance of work relating to a relevant contract… are taken to be wages paid or payable during that financial year”. The Supreme Court had previously determined that “payment” did not extend to the return of money from one person to another. Therefore, because the Optometrist Entities derived the amounts, and they were held on trust for them, that there was no payment and payroll tax did not apply.

The Victorian Court of Appeal ultimately found that:

The ordinary meaning of “payment” under the payroll tax provisions includes a payment of money to a person already beneficially entitled to that money.

This satisfied the meaning of the Optometrist Entities being “paid” amounts by the Trustee within the meaning of the payroll tax provisions.

There was no perceived basis upon which it could be said that the distributions in questions were not “amounts paid or payable” by an employer for or in relation to the performance of work, however the parties were provided an opportunity to make further submissions on this point.

This decision is a contentious one as the payroll tax provisions were interpreted broadly such to override the legal realities and existence of a trust. It has clearly been acknowledged that the Optometrist Entities do have a real and existing beneficial entitlement to the money, and despite this, is still being charged payroll tax for the moneys being transferred back to them.

This decision could potentially have wide ranging effect to situations where payments are made through intermediaries. This could include, for example:

The payment of a real estate agent’s commission by a vendor from a lawyer’s trust account;

They payment of a one professional’s fees by another professional on behalf of a client – such as lawyers paying for valuers or accountants paying for legal services as a disbursement for their clients.

If such situations were found to be payments for or in relation to work, then, unless one of the “contractor’s exemptions” applied, the amount will be subject to payroll tax.

As a result of the Victorian Court of Appeal’s decision, the payroll tax clampdown against the healthcare industry is anticipated to continue.

If you have any questions, please contact our specialist team at:

Denise Tan

Senior Associate

T +61 3 9611 0160 | M +61 438 714 965

E: dtan@sladen.com.au

Phil Broderick

Principal

T +61 3 9611 0163 l M +61 419 512 801

E: pbroderick@sladen.com.au

Laura Spencer

Senior Associate

T +61 3 9611 0110

lspencer@sladen.com.au