Landholder duty – Part 7 – Exemptions

Landholder duty is a regime that was introduced to impose duty on acquisitions in landholding entities. These complicated provisions are difficult to understand, and yet are increasingly becoming a compliance area of focus for revenue authorities. This is Part 7 of a series of articles by our State Taxes Team on landholder duty and deconstructs the complex provisions by providing a snapshot on landholder duty and its application with regards to private entities.

In Parts 1 to 6 of our landholder duty article series, we discussed the different ways landholder duty can arise under the landholder regimes. In this final article, we discuss the exemptions that may apply, with a particular focus on the Victorian duty provisions.

Exemptions

Various exemptions from landholder duty are available pursuant to section 89D of the Duties Act 2000 (Vic) (Act).

Notably, where there is a pro-rata increase of interests held by all the unit or share holders in a landholder, an exemption from duty applies under sub-section 89D(d) of the Act.

While there are varying opinions as to whether a pro-rata increase of interest in a landholder constitutes an acquisition of units/shares in the first place, the Victorian State Revenue Office’s view is that it does. While this may not matter for the pro-rata acquisition (which is exempt under sub-section 89D(d)) that acquisition could be counted under the aggregation rules (as discussed in Part 3 of our landholder series).

Duty exemptions that are available under Chapter 2 of the Act (i.e. that apply to direct transfers of land) also apply to relevant acquisitions of interest in a landholder. Sub-section 89D(a) of the Act operates to fully exempt a relevant acquisition from landholder duty if the transfer would have otherwise been exempt if it was a transfer of land.

Anomalous duty outcome

Under section 89E of the Act the Commissioner may reduce duty payable to an amount not less than the duty that would be payable under Chapter 2, had the subject of the acquisition been a transfer of the land of the landholder to the person.

This could apply, for example, where a dealing in relation to units or shares is greater than the interests in the underlying interests in the land of the landholder.

Examples of available exemptions

Common examples where full or partial exemptions may be available for dutiable relevant acquisitions comprising of transfer/s in a landholder include:

A transfer that occurs due to a change of trustees.

A transfer from a fixed trust or a discretionary trust to beneficiaries of the trust.

A transfer from one superannuation fund to another, or to trustees or custodians of superannuation funds.

A transfer from a superannuation fund to a beneficiary of the fund.

A transfer that occurs due to distributions under a deceased estate.

Transfer/s to relatives involving underlying land holdings which comprise of land that qualify for a primary production exemption from land tax.

Transfers that are exempt from duty under the corporate reconstruction or consolidation provisions. These provisions provide exemptions for transfers within wholly owned corporate groups or an interposition of a new head co to create an income tax consolidated group.

It is noted that the above list is not exhaustive but rather is indicative of the types of exemptions that could be available. The provisions within the Act contain specific requirements to qualify for a particular exemption, and legal advice should be sought where seeking to apply these exemptions.

Example

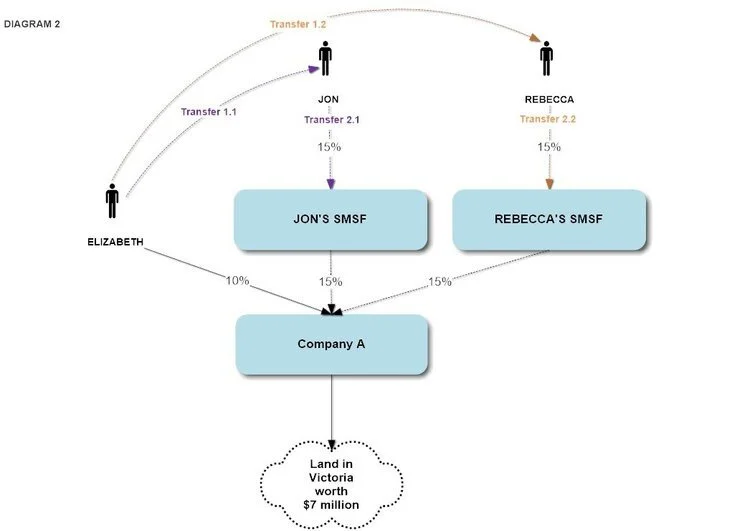

To demonstrate how an exemption would practically work, we refer back to the example set out in in Diagram 2, Part 4 of our series here:

Elizabeth is considering her portfolio and decides to gift 15% of her share in Company A to her husband Jon (Transfer 1.1) and 15% to her niece Rebecca (Transfer 1.2). As outlined in Part 4 of our series, each of Transfer 1.1. and 1.2 are subject to duty with no available duty exemptions.

Following this, both Jon and Rebecca decide to transfer their share to their relevant self-managed superannuation funds (SMSF) (otherwise identified as Transfer 2.1 and Transfer 2.2 respectively). This is permitted under the superannuation laws as the Company A satisfies the requirements of regulation 13.22C of the Superannuation Industry (Supervision) Regulations 1994.

Pursuant to the application of sections 89D and 41 of the Act no duty is chargeable in respect of Transfer 2.1 and 2.2 if the means by which each of the Jon’s SMSF and Rebecca’s SMSF acquired 15% of the shares in Company A would have otherwise not been subject to duty due to an exemption applying under Chapter 2 (such as section 41 of the Act).

In this circumstance each of the transfers occurred without consideration to a trustee of a complying superannuation fund (each of Jon’s SMSF and Rebecca’s SMSF) where there is no change in the beneficial ownership of shares being transferred. Therefore, the transfers should be exempt from duty. It is noted however that the interests acquired by the SMSFs may still be subject to the aggregation rules as discussed in Part 4 of this series.

Where the transfer involves units or shares in a landholding entity, it is best practice that each transfer and resulting increase in the particular member or beneficiary’s account in the SMSF is correctly documented.

If you have any further questions on the application of landholder duty or state taxes, please contact one of the members of our specialist team:

Denise Tan

Senior Associate

T +61 3 9611 0160 | M +61 438 714 965

E: dtan@sladen.com.au

Laura Spencer

Senior Associate

T +61 3 9611 0110

lspencer@sladen.com.au

Phil Broderick

Principal

T +61 3 9611 0163 l M +61 419 512 801

E: pbroderick@sladen.com.au