Landholder duty – part 3 – the aggregation rules

Landholder duty is a regime that was introduced to impose duty on acquisitions in landholding entities. These complicated provisions are difficult to understand, and yet are is increasingly becoming a compliance area of focus for revenue authorities. This is Part 3 of a series of articles by our State Taxes Team on landholder duty and deconstructs the complex provisions by providing a snapshot on landholder duty and its application with regards to private entities.

Introduction

It is reasonably well known that a transfer of a ‘significant interest’ in a landholder may trigger a landholder duty liability. What is less well known is how the aggregation rules can cause what would otherwise be non-dutiable transfers to be dutiable or result in additional duty being triggered.

The unexpected application of the aggregation rules can result in costly and surprising duty liabilities for taxpayers. With the increased investigation and monitoring activities undertaken by revenue offices throughout Australia, it is important that taxpayers are familiar with these provisions.

The Aggregation Rules

The landholder duty provisions are contained within all duty legislation throughout Australia. The further acquisition and aggregation principles within this legislation can deem separate transactions to be a relevant acquisition subject to landholder duty. As a result, individual transactions which by themselves are below the significant interest threshold, can be aggregated with other interests and result in exceeding the significant interest threshold.

In all jurisdictions other than the Northern Territory and South Australia, the aggregation provisions will apply where one or more transactions form substantially one arrangement. See: section 25 Duties Act 1997 (NSW), section 30 Duties Act 2001 (QLD), section 24 Duties Act 2000 (VIC), section 37, Duties Act 2008 (WA), section 24 Duties Act 1999 (ACT) and section 22 Duties Act 2001 (TAS).

In the Northern Territory (see section 52A Stamp Duty Act (NT)) and South Australia (see section 67(4) Stamp Duties Act 1923 (SA)) the provisions focus on interrelated instruments and whether, together, they form or arise from, substantially one transaction or one series of transactions, of the same dutiable property.

Understanding the concept of what amounts to a relevant acquisition by way of aggregating a series of transactions is key to understanding when the provisions will apply in each of the jurisdictions. However, in doing so consideration needs to be given to the specific interpretations made by each relevant revenue office in relation to forming one arrangement, transaction or series of. For the purpose of this article we will examine how the principles operate in Victoria.

Under section 78 of the Duties Act 2000 (Vic), a person who acquires:

20% or more of the units in a private unit trust; or

50% or more in a private company;

that holds land in Victoria with a value greater than $1 million will make a relevant acquisition subject to landholder duty.

Whether an acquisition exceeds the 20%/50% relevant threshold is not only measured against the acquisition by the purchaser in a landholder, it is also measured against three aggregation rules:

aggregation of prior acquisitions by the person;

aggregation of acquisitions by associated persons; and

aggregation of acquisitions that comprise an associated transaction.

Prior acquisitions by a person

A prior acquisition made by a person may be aggregated with a new interest to determine whether the threshold is breached. This prior acquisition may have been exempt at that earlier time (for example where the entity was not a landholder at the time) but may be included in determining whether duty is now payable (though that portion will remain exempt).

It is noted that the 3-year aggregation rule that formerly applied under the previous land rich provisions has now been removed. All acquisitions are taken in account in determining whether a relevant acquisition has been made, however duty is calculated only by reference to interests acquired within 3 years from the date of the relevant acquisition.

Associated persons

Generally, under section 78(1)(a)(ii)(B), acquisitions will be aggregated where the acquirers are associated persons (broadly, related persons and/or entities). An associated person is widely defined under section 3(1) and can include relatives; related bodies corporate, trustees or companies; partners in a partnership and associated persons of associates.

Associated transaction

In addition, to aggregating acquisitions by the purchaser and by associated persons, acquisitions by unrelated persons in an associated transaction will also be aggregated where it can be determined that:

the persons are acting in concert; or

the acquisitions form, evidence, give effect to or arise from substantially one arrangement, one transaction or one series of transactions.

To be acting in concert there must be at least an understanding between the persons as to a common purpose or objective.

When considering whether acquisitions of interests in a landholder constitute ‘substantially one arrangement, one transaction or one series of transactions’, the Commissioner will look at the substance of the acquisitions and whether there is some unity, oneness or unifying factor between the acquisitions.

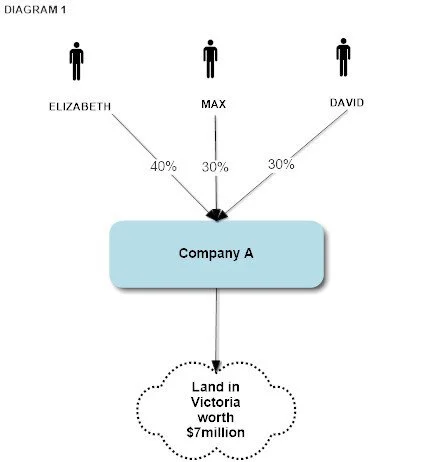

Example

In Diagram 1, Elizabeth, Max and David (all unrelated) acquire interests in Company A, a landholder in Victoria. Each interest is less than 50% and therefore are not, in their own right, a significant acquisition in a landholder. Without any further investigation, each acquisition on itself would not be subject to duty.

Notably, no party has made a prior acquisition in the company, therefore the acquisitions will not be aggregated under the prior interest rules. Further, as Elizabeth, Max and David are unrelated, their acquisitions will not be aggregated under the associated person rules.

However in order to properly assess the duty liability of each of Elizabeth, Max and David’s acquisitions, consideration should be given to whether the three transactions are related. As noted above this will involve consideration of whether the parties acted in concert or whether their acquisitions form substantially one arrangement, one transaction or one series of transactions.

Further facts

Acting in Concert

Upon further investigation into Example 1 it is understood that David was advised by his financial advisor that Company A was for sale. David, unable to fund the acquisition completely by himself, contacted his acquaintances, Elizabeth and Max informing the opportunity to buy into the company. Given that David is buying into the company both Elizabeth and Max agree to purchase 40% and 30% of the shares in the company. David then facilitates their introduction to the seller.

Here, there is an understanding between the parties and a common purpose. Despite not acquiring significant interests in their own right, as they were acting in concert, their acquisitions will be aggregated and deemed to be an aggregated acquisition of 100% in Company A, resulting in a duty liability of $385,000.

Substantially one arrangement, one transaction or one series of transactions

In the example, if we return to the original fact that the three purchasers did not know one another prior to the acquisition; David offers to buy 30% of Company A from the seller. The seller advises him that it will only sell 100% of the company. The seller’s agent engages in negotiations with Elizabeth and Max to acquire the remaining 70%. Each party agrees to acquire their relevant percentage conditional on acquisitions being made by the other two parties. Due to the interdependency between the contracts and the joint negotiations, the acquisitions would form one arrangement, one transaction or one series of transactions. The resulting duty liability would be $385,000.

The examples above are a simplified application of the complex aggregation rules. In Part 4 of this series we will discuss the traps that can occur when the same interest is transferred multiple times.

In practice the scenarios may not be as straight forward as those outlined above and advisors should therefore carefully consider the application of the aggregation rules. If you have any questions on the application of landholder duty or state taxes, please contact one of the members of our specialist team:

Laura Spencer

Senior Associate

Sladen Legal

T +61 3 9611 0110

Level 5, 707 Collins Street, Melbourne, 3008, Victoria, Australia

lspencer@sladen.com.au

Denise Tan

Senior Associate

Sladen Legal

T +61 3 9611 0160 | M +61 438 714 965

Level 5, 707 Collins Street, Melbourne, 3008 Victoria, Australia

E: dtan@sladen.com.au

Phil Broderick

Principal

Sladen Legal

T +61 3 9611 0163 l M +61 419 512 801

Level 5, 707 Collins Street, Melbourne, 3008, Victoria, Australia

E: pbroderick@sladen.com.au