Landholder duty – part 4 –aggregation and the double counting “trap”

Landholder duty is a regime that was introduced to impose duty on acquisitions in landholding entities. These complicated provisions are difficult to understand, and yet are increasingly becoming a compliance area of focus for revenue authorities. This is Part 4 of a series of articles by our State Taxes Team on landholder duty and deconstructs the complex provisions by providing a snapshot on landholder duty and its application with regards to private entities.

Introduction

In Part 3 of our landholder duty article series, we discussed the principles of aggregation under the landholder regimes. In this article, we discuss the traps that can occur when the same interest is transferred multiple times. Advisors and taxpayers should be mindful of transactions which involve multiple transfers, especially when exempt transactions are or have been involved. A closer look may be required to determine whether the aggregation principles may apply. Without vigilant consideration unexpected duty liabilities may arise.

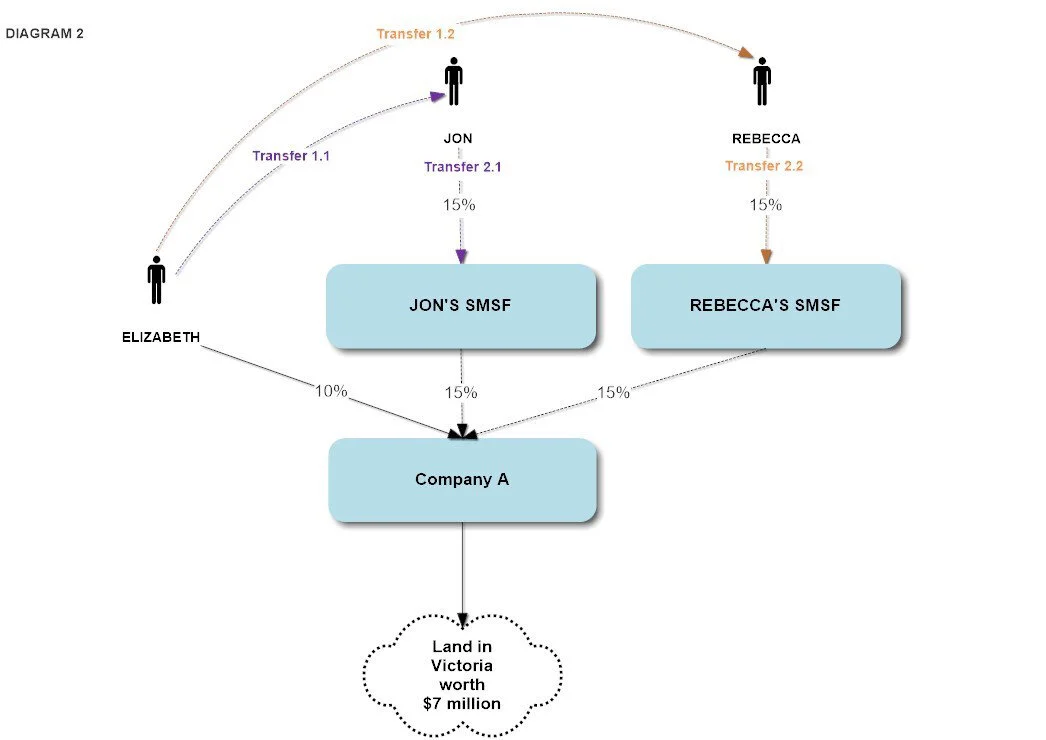

Following on from the example outlined in Part 3 we revisit the example of Elizabeth and again focus on the Victorian duty provisions. Four years after her acquisition in Company A Elizabeth is considering her portfolio and decides to gift 15% of her share in Company A to her husband Jon (Transfer 1.1) and 15% to her niece Rebecca (Transfer 1.2). Both Jon and Rebecca decide to transfer their share to their relevant self managed superannuation funds (SMSF) (otherwise identified as Transfer 2.1 and Transfer 2.2 respectively) – as permitted by the superannuation laws in certain circumstances. This is shown below in Diagram 2.

What may appear to be two distinct acquisitions by Jon and Rebecca, and what is clearly only the movement of an underlying 30% interest in Company A, will, following the Supreme Court of Victoria decision of Razzy Australia Pty Ltd & Anor v Commissioner of State Revenue [2021] VSC 124 (Razzy) in fact be deemed to be an aggregated acquisition of 60% in Company A and therefore subject to duty. The 60% aggregated acquisition is determined as follows:

15% acquisition by Jon (Transfer 1.1);

15% acquisition by Jon’s SMSF (Transfer 2.1);

15% acquisition by Rebecca (Transfer 1.2); and

15% acquisition by Rebecca’s SMSF (Transfer 2.2).

Following the Victorian Supreme Court’s decision in Razzy, any changes in equitable ownership ‘however achieved’ are calculated for the purposes of the aggregation provisions. Therefore, exempt acquisitions are counted for determination whether a significant interest is acquired, even though the exempt acquisitions are themselves not dutiable.

In the example outlined, whilst the transfers to the trustees of the SMSFs would be exempt under the Victorian duties legislation, the Victorian Commissioner will still include exempt amounts when calculating the total aggregated acquisition. In the present example, these exempt transfers will not be subject to duty, however the remaining 30% will be subject to a duty liability of $115,500. Taxpayers will also need to consider factors as identified in Revenue Ruling DA.057 to better identify any landholder duty liabilities with reference to the Victorian provisions, such as whether the acquirers were acting in concert, if the acquisitions (in form or evidence) give effect to or arise from substantially one arrangement, one transaction or one series of transactions, if the interest acquired will be used independently, if negotiations were conducted separately and if there is a common purpose or oneness for the transactions.

If you have any further questions on the application of landholder duty or state taxes, please contact one of the members of our specialist team:

Laura Spencer

Senior Associate

Sladen Legal

T +61 3 9611 0110

Level 5, 707 Collins Street, Melbourne, 3008, Victoria, Australia

lspencer@sladen.com.au

Denise Tan

Senior Associate

Sladen Legal

T +61 3 9611 0160 | M +61 438 714 965

Level 5, 707 Collins Street, Melbourne, 3008 Victoria, Australia

E: dtan@sladen.com.au

Phil Broderick

Principal

Sladen Legal

T +61 3 9611 0163 l M +61 419 512 801

Level 5, 707 Collins Street, Melbourne, 3008, Victoria, Australia

E: pbroderick@sladen.com.au