Super guarantee Series - Part 4: How is super guarantee and the super guarantee charge calculated?

In Part 1 of our Super Guarantee article series, we discussed the background to the super guarantee regime and an overview of how the regime operates. In Part 2, we looked at who will be covered by the super guarantee regime, and in Part 3 we specifically looked at when this will include certain contractors.

Now in Part 4, we explain how super guarantee (SG) and the SG charge are calculated, with reference to the key concepts of ‘ordinary time earnings’ and ‘salary and wages’.

Ordinary time earnings

Under section 19(2) of the Superannuation Guarantee (Administration) Act 1992 (SG Act), the minimum contribution to superannuation an employer must pay for each eligible employee is currently 10.5% of their ‘ordinary time earnings’ (OTE). This is the SG and must be paid quarterly.

This prompts the question – what is included in OTE?

OTE is defined under section 6(1) of the SG Act as follows:

ordinary time earnings, in relation to an employee, means:

(a) the total of:

(i) earnings in respect of ordinary hours of work other than earnings consisting of a lump sum payment of any of the following kinds made to the employee on the termination of his or her employment:

(A) a payment in lieu of unused sick leave;

(B) an unused annual leave payment, or unused long service leave payment, within the meaning of the Income Tax Assessment Act 1997; and

(ii) earnings consisting of over‑award payments, shift‑loading or commission; or

(b) if the total ascertained in accordance with paragraph (a) would be greater than the maximum contribution base for the quarter—the maximum contribution base.

The SG Act does not define the expression ‘earnings in respect of ordinary hours of work’ or any of the terms in that expression.

The definition of OTE under 6(1) of the SG Act specifically excludes the following from being OTE:

A lump sum payment of any of the following kinds made to the employee on the termination of his or employment:

a. a payment in lieu of unused sick leave;

b. an unused annual leave payment, or unused long service leave payment.

SGR 2009/2

Superannuation Guarantee Ruling 2009/2 (SGR 2009/2) sets out the ATO view on the meaning of OTE as defined in section 6(1) of the SG Act. It also sets out the ATO view on the meaning of ‘salary and wages’ as defined in section 11 of the SG Act (which is relevant for the calculation of the SG shortfall and SGC, as discussed below).

Importantly, SGR 2009/2 confirms that OTE does not include overtime. Therefore, SG, if paid on time, will typically not be calculated in relation to overtime.

Specifically, paragraphs 13 and 15 provide as follows:

13. An employee’s ordinary hours of work’ are the hours specified as his or her ordinary hours of work under the relevant award or agreement, or under the combination of documents, that governs the employee’s conditions of employment.

15. Any hours worked in excess of, or outside the span (if any) of, those specified ordinary hours of work are not part of the employee’s ‘ordinary hours of work’.

A common question that is asked is whether OTE includes commission paid to an employee.

The ATO confirms in SGR 2009/2 that OTE will typically include commission, unless that commission is in respect of overtime:

23. A commission is a payment made to an employee such as a salesperson on the basis of the volume of sales he or she achieves or other similar criteria. These are always OTE except in the unusual case where they can be shown to be wholly referable to overtime hours worked.

SGR 2009/2 also confirms that other specific kinds of payments are OTE (unless they relate to overtime):

allowances and loadings (eg, a ‘casual loading’ of 20% of the basic ordinary time rate of pay paid to a casual worker in lieu of any fixed, regular minimum hours of work and of paid leave entitlements);

bonuses (except for, eg, a discrete and clearly identifiable bonus payment that relates solely to work performed entirely outside ordinary hours);

piece rates;

paid leave and holiday pay;

payments in lieu of notice;

directors’ fees.

Maximum contribution base

The total of OTE in respect of an employee for a quarter cannot exceed the maximum contribution base for a quarter due to the definition of OTE under section 6(1) of the SG Act.

That is, the maximum contribution base places a maximum limit on any individual employee’s earnings base for each quarter of any financial year. Employers do not have to provide the minimum support for the part of earnings above this limit.

The maximum contribution base for the 2022-23 income year is $60,220 per quarter. Therefore, for the current income year, where an employee receives more than $60,220 per quarter in total OTE, the employer must only pay SG on $60,220 (ie, 10.5% x $60,220 = $6,323.1).

When must contributions be made?

To avoid late payments (and therefore avoid triggering the SGC), SG contributions must be made quarterly, within 28 days after the end of the relevant quarter as shown:

Employers and employees can contractually agree to make SG contributions more frequently than quarterly, for example fortnightly or monthly. If they do, the employer must ensure the total SG contribution for each quarter is made by the due date.

Late or underpaid SG and the SGC – how is it calculated?

If employers fail to make the minimum SG contributions for eligible employees by the quarterly deadline, they will be liable to pay the SG charge (SGC) under sections 17 and 46 of the SG Act. The SGC is a penalty amount which is payable by the employer to the ATO and is additional to any unpaid SG. That is, as can be seen below, the SGC will always be higher than the SG that would have been payable if the contributions were made in full and on time. In addition, the SGC is not tax deductible to the employer.

SGC is made up of three parts:

the amount representative of superannuation the employee was owed and not paid (Shortfall Amount);

interest on the Shortfall Amount; and

an administration fee (payable for each employee).

As the SGC scheme is self-assessed, employers need to report and correct any missed SG payments themselves and lodge an SGC statement under section 33 of the SG Act. To lodge the SGC statement, employers will need to calculate the SGC, including the Shortfall Amount.

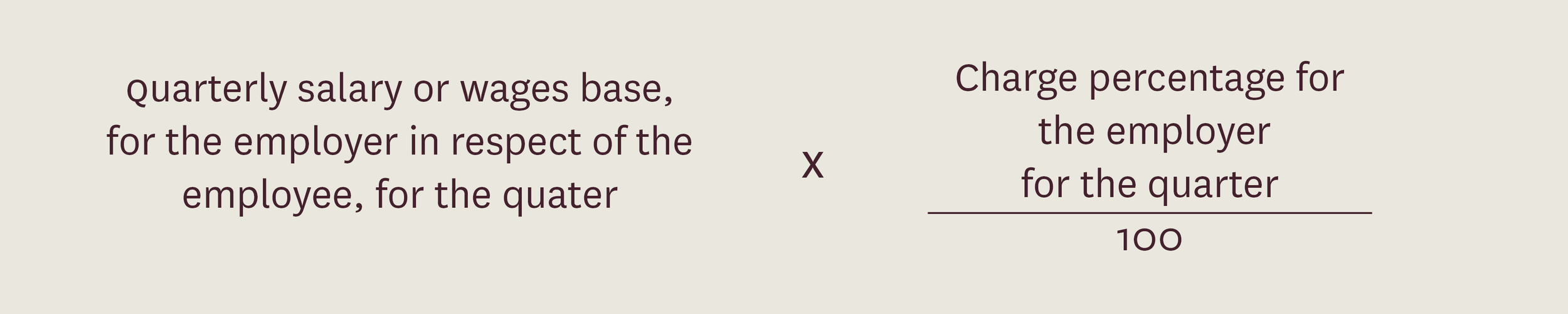

The Shortfall Amount

The Shortfall Amount is not equal to the amount of SG that the employee was owed but not paid, it is a separately calculable sum which relies on different amounts to the SG calculation.

The shortfall amount is worked out using the following formula under section 19(1) of the SG Act:

The “quarterly salary or wages base” is the total ‘salary or wages’ paid by the employer in respect of the employee for the quarter, including any salary sacrificed amounts. The ‘charge percentage’ for the quarter is the number specified in section 19(2) of the SG Act.

Conversely, the SG (ie, when paid on time), is simply the “charge percentage” (currently 10.5%) of an employee’s OTE.

The main distinction is that the Shortfall Amount is largely based on “salary or wages” and the SG is dependent on OTE. However, in some circumstances, both amounts are necessary to calculate the Shortfall Amount.

Although they are interrelated concepts, OTE and “salary or wages” are not interchangeable terms and represent different amounts earned by employees.

The ATO note in SGR 2009/2 at paragraph 60 that when determining what classifies as “salary or wages” the ordinary meaning of the term is applied, being remuneration paid to employees for their services as employees. The SG Act also provides specifically included and excluded amounts.

‘Salary or wages’ are defined under section 11 of the SG Act to include:

commission;

payments made to body corporate executives;

payments for the labour component of a contract which is principally for the labour of a person;

payments to members of Parliament;

payments to performers (for example, dancers, artists and actors); and

public office holder remuneration.

That is, ‘salary or wages’ is broader than OTE and includes the entirety of OTE in addition to other amounts.

Importantly, payments for overtime hours are “salary or wages”. Overtime payments fit within the ordinary meaning of “salary or wages”, as these payments are a reward to employees for their services as employees, and such payments are not specifically excluded by the SG Act as “salary or wages”.

Other components of SGC

In addition to the Shortfall Amount, the SGC includes:

“nominal” interest of 10% per annum (accrues from the start of the relevant quarter);

an administration fee of $20 per employee, per quarter.

When is SGC due?

SGC is due 28 days in the second month following the end of the relevant quarter as shown below:

To whom must the SGC be paid?

Where SG contributions are made on time for the relevant quarter, they should be made directly to the employee’s super fund (or qualifying clearing house). Where SG contributions are late, and SGC is payable, the SGC should be paid to the ATO.

Of that SGC paid to the ATO:

the Shortfall Amount and notional interest will be transferred by the ATO to the employee’s super fund and counted as a contribution under their concessional contributions cap;

the administration fee is retained by the ATO/Government.

SG audits – how far back can the ATO go?

Technically, there is no statutory limit on how far back the ATO can review when conducting SG audits and issuing amended notices of assessment. In theory, therefore, an audit could review as far back as 1992 when the SG regime first began. In practice, however, the ATO typically only go back four years, unless their compliance action was prompted by a particular employee complaint. In that case, they may go back to the commencement of the particular working engagement, even if that is more than four years ago.

Choice shortfall and other penalties

Where employers do not give eligible employees a choice of super fund, the ‘choice liability’ may apply.

A choice liability penalty will apply where employers:

do not give their employees a superannuation standard choice form within the requirement timeframe;

pay their eligible employees’ super to a complying fund but not the fund they chose;

charge their employees a fee for implementing their choice of fund.

The choice liability penalty increases the SG as follows:

prior to 1 November 2021 – 25% of the notional quarterly shortfall;

post 1 November 2021, including failure to comply with the stapled fund requirement – 100% of the notional quarterly shortfall.

Other penalties which may apply in addition to the SGC are:

administrative penalties for making false or misleading statement on SG statements – penalty of up to 75% of the shortfall;

general interest charge (GIC) on SGC not paid by the due date;

failure to keep adequate records – maximum fine of 30 penalty units (currently $6,600);

failure to provide an employee’s TFN – maximum fine of 10 penalty units (currently $2,200).

* * * * *

If you have any questions about how super guarantee should apply in your circumstances, please contact our specialist team at:

Phil Broderick

Principal

M +61 419 512 801 | T +61 3 9611 0163

E: pbroderick@sladen.com.au

Philippa Briglia

Senior Associate

T +61 3 9611 0173

E pbriglia@sladen.com.au

Jan Oh

Graduate Lawyer

T +61 3 9611 0158

E joh@sladen.com.au