Capital gains, discretionary trusts, and foreign residents – round 2 to the ATO

We wrote here on the decision of Thawley J of the Federal Court in Peter Greensill Family Co Pty Ltd (trustee) v FCT (Greensill) where the Commissioner of Taxation was successful in arguing that section 855-10 of the Income Tax Assessment Act 1997 (ITAA 1997) does not disregard a capital gain distributed to a foreign resident beneficiary of an Australian discretionary trust. The taxpayer has appealed that decision to the Full Federal Court.

Steward J of the Federal Court recently considered similar circumstances in N & M Martin Holdings Pty Ltd v FCT [2020] FCA 1186 (Martin). In Martin, in the years of income ended 30 June 2013 and 2014, the trustee for the Martin Family Trust (Trust), an Australian discretionary trust, sold shares, not being ‘taxable Australian property’, in a company. The Trust distributed capital gains from those share sales to a discretionary object of the Trust who was not an Australian tax resident.

As in Greensill, in Martin:

the Trust and discretionary object said that section 855-10 applied to disregard the capital gains; and

the Commissioner said that section 855-10 did not work to disregard the capital gains.

Steward J in Martin followed Thawley J in Greensill and, while finding the taxpayer’s arguments “rational and thoughtful”, found for the Commissioner saying:

... Greensill is ... a very well-reasoned judgment that traverses all of the relevant statutory and extrinsic materials that bear upon the correct construction of s. 855-10. It reaches a logical conclusion after detailed analysis of the language of that provision, statutory context, and legislative history. ... [I]t is the subject of an appeal to the Full Court ... In such circumstances, as a matter of precedent, comity and good sense, in my view I should follow it as a trial judge. ... [T]hat is all the more important in the field of taxation law, being a national law that affects all Australians ....

Martin (and Greensill) considered the interaction of trust taxation rules in Division 6 and Subdivision 6E of the Income Tax Assessment Act 1936, Subdivision 115-C of the CGT rules in the ITAA 1997, and Division 855 of the ITAA 1997 about capital gains and foreign residents. Those rules, and interactions, are complicated.

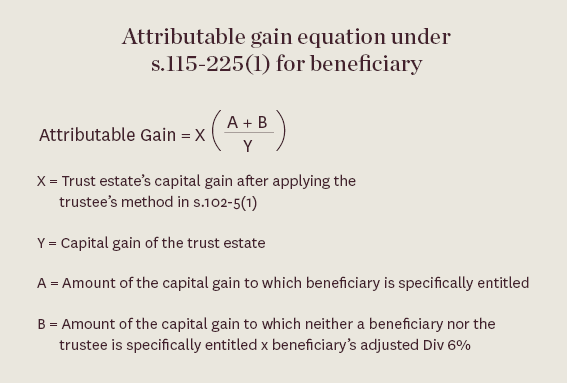

Senior Counsel for the Commissioner supplied a formula to Steward J to illustrate the operation of Subdivision 115-C.

Steward J said:

Whilst this formula was helpful to me, assisted as I was by the explanation given about it by Mr. O’Meara, Senior Counsel for the Commissioner, it may be doubted whether the average Australian, who may not be able to secure Mr. O’Meara’s help, could easily or ever apply it.

Whether the taxpayer in Martin intends to appeal is unknown. However, as the taxpayer in Greensill has appealed there is at least one more round of this fight over the application of Australia’s capital gains tax rules and section 855-10 remaining. Watch this space! As Steward J said “… the case the applicants advance would, one might think, be likely to enhance “Australia’s status as an attractive place for business and investment”, which is one of the “objects” of [Division 855]”.

For more information please contact:

Neil Brydges

Principal Lawyer | Accredited Specialist in Tax Law

M +61 407 821 157 | T +61 3 9611 0176

E nbrydges@sladen.com.au

Lucy Liang

Graduate Lawyer

E lliang@sladen.com.au