A Guide To Understanding Payroll Tax Part 1: The Basics

WHAT IS PAYROLL TAX?

Payroll tax is a state and territory tax. It is assessed where total Australian taxable wages paid or payable to employees by an employer exceed specific thresholds. The tax is self-assessed and as such the obligation falls to employers to ensure they are aware of their total wage bill across Australian states and territories and whether those are taxable.

Each state and territory has its own payroll tax legislation and related rulings. To address the confusion and complexity created by the many variations between the provisions the Commissioners from each state and territory in 2007 commenced a harmonisation process. The purpose of this was to align key areas of the payroll tax provisions and have greater administrative consistency. Some areas continue to differ between the states and territories, therefore ensuring a careful consideration each relevant jurisdiction is vital.

In Victoria, which will be the main focus of this series, the legislation is provided for in the Payroll Tax Act 2007 (PTA 2007) and is administered by the Victorian State Revenue Office.

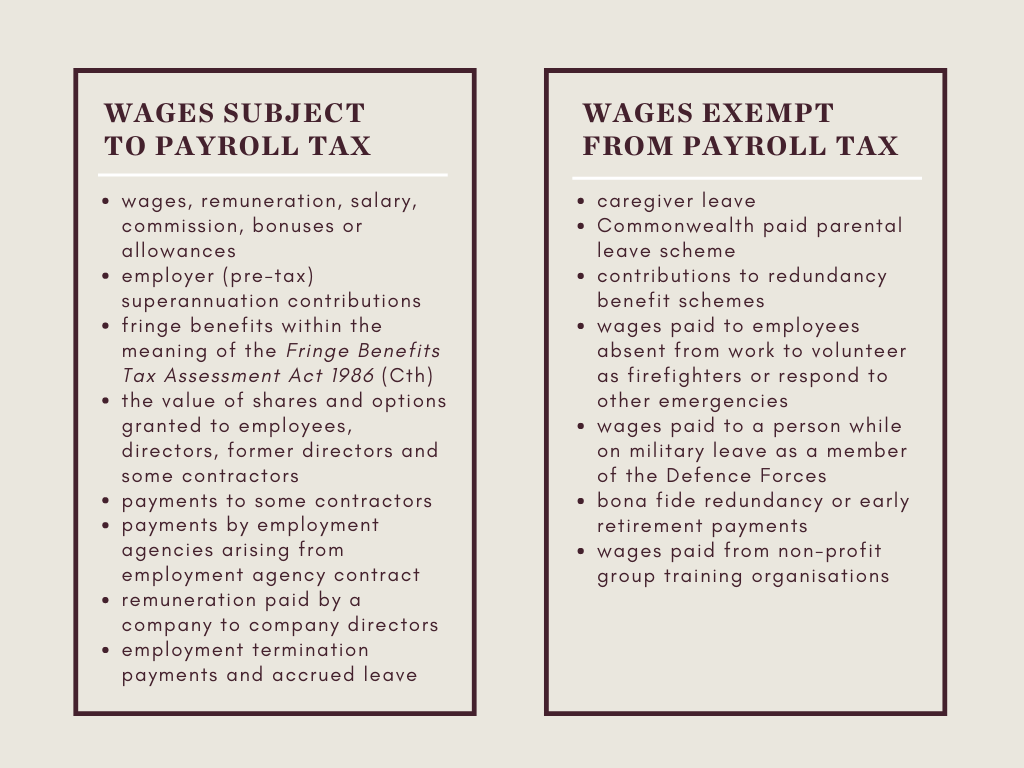

WHAT ARE WAGES?

As noted above, payroll tax is assessed on Australian taxable wages. Whilst the geographical location is relatively self-explanatory (i.e. the wages must be paid in Australia), what constitutes ‘wages’ needs further consideration. In Victoria wages are taken to include, and exclude, the following amounts:

WHEN DOES PAYROLL TAX APPLY TO WAGES PAID?

Payroll tax only applies to taxable Australian wages. Generally, ‘taxable wages’ can be split in to three types of payments. These are as follows:

1. Wages paid/payable from employer to a common law employee

‘Employee’ is not defined in the PTA 2007 and therefore takes its ordinary or common law meaning. Common law principles for determining whether a worker is an employee have been developed by the courts over time. Several factors, which should be considered in totality, have been deemed by the courts as demonstrating whether an employee / employer relationship exists. These factors include:

control and direction of the employer over the worker;

contract terms versus practical relationship;

whether the engagement contract is to achieve a ‘given result’ or labour;

if the individual runs an independent business;

if the worker has the power to delegate;

who carries the risk;

who provides tools and equipment; and

other factors as the Commissioner may consider.

2. Payments to certain contractors

The purpose of the payroll tax contractor provisions is to impose payroll tax on payments made to contractors that do not fall within the 6 contractor exclusions. This will be discussed in further detail in part 5 and 6 of this series.

3. Employment agencies

Any amount paid or payable by an employment agent under an employment agency contract will be subject to payroll tax. This will also be discussed in further detail in part 7 of this series.

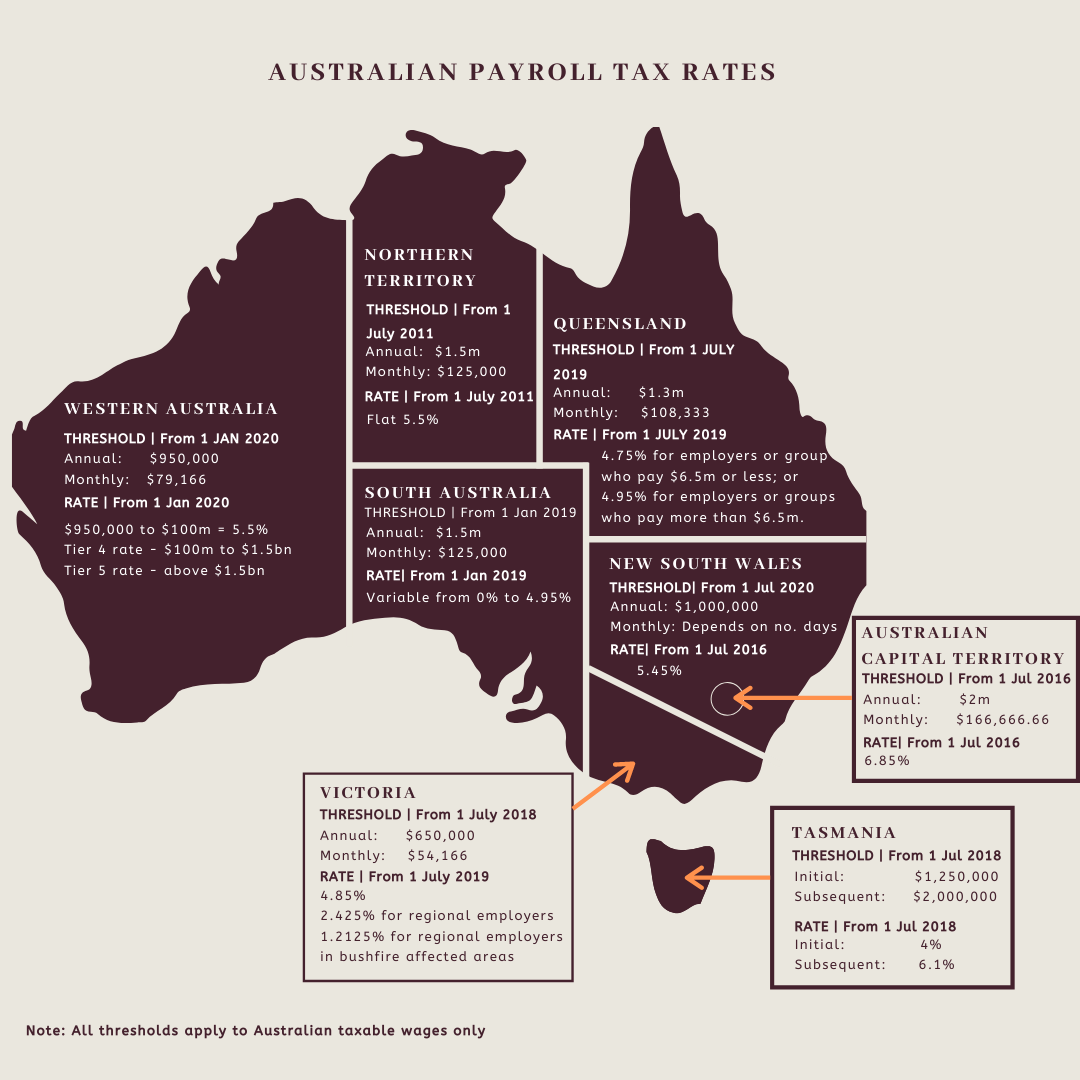

How Much Payroll Tax Is Payable?

Each state and territory set their own rates of payroll tax and the thresholds which must be surpassed for payroll tax to be payable. At the time of writing, the applicable rates and thresholds are as follows:

In relation to the above rates and thresholds, it is noted:

The payroll tax thresholds can be apportioned where you are not an employer for an entire year.

The above rates and thresholds may be affected by state and territory measures to assist businesses with the impact of COVID-19 and the Australian bushfires. For more details see here.

Do I need to Register?

Generally, if you are an employer paying wages in Australia, and your taxable wages exceed the applicable monthly threshold set by that jurisdiction (though based on total Australian wages), then you must register with the revenue office in that state or territory. This must be done even where you think the annual threshold may not be exceeded.

Employers which are members of a group should be mindful that one threshold applies to the whole group, rather than to each member.

Questions?

If you have any questions about how payroll tax should apply in your circumstance, please contact our specialist team at:

Laura Spencer

Senior Associate

T +61 3 9611 0110

lspencer@sladen.com.au

Denise Tan

Senior Associate

T +61 3 9611 0160 | M +61 438 714 965

E: dtan@sladen.com.au

Phil Broderick

Principal

T +61 3 9611 0163 l M +61 419 512 801

E: pbroderick@sladen.com.au