Payroll Tax Series – Part 10 – Payroll Tax Grouping

In this 10th part of our payroll tax series, we explore the grouping provisions contained in the Payroll Tax 2007 (PTA 2007). While we will refer to the Victorian legislation, similar provisions exist in all states and territories due to a harmonisation of the law.

What is payroll tax grouping?

The grouping provisions were introduced across Australia to address the practice of tax avoidance by creating multiple entities for employing staff in what was still effectively the same business. By having distinct entities each was able to claim a separate payroll tax threshold meaning that they were able to minimise or completely avoid paying payroll tax.

The grouping tests

The grouping provisions group entities that are deemed to be one business and provide a single threshold deduction for the group. Part 5 of the PTA 2007 provides four tests, under any of which, entities will be grouped. Those tests are:

the entities are corporations which are related to each other by virtue of section 50 of the Corporations Act – being the holding company and subsidiary relationship;

the entities share at least one employee;

the entity has a controlling interest in a corporation as a result of tracing interests in corporations; or

the same person, or set of persons, has a controlling interest in the two entities.

We discuss each of these in further detail below.

Test 1 - Related entities

Corporations will be grouped under section 70 of the PTA 2007 where they are related bodies corporate within the meaning of section 50 of the Corporations Act. Pursuant to section 50 of the Corporations Act where a body corporate is a holding company of another body corporate, a subsidiary of another body corporate or a subsidiary of a holding company of another body corporate then the first mentioned body and the other body will be deemed to be related to each other.

These definitions are complex but broadly a subsidiary company includes a company that is controlled by another company (the holding company) under the following three tests:

The holding company controls the subsidiary company’s board (control being broadly defined);

The holding company can cast more than 50% of the shareholding voting rights in the subsidiary company; or

The holding company holds more than 50% of the share capital in the subsidiary company.

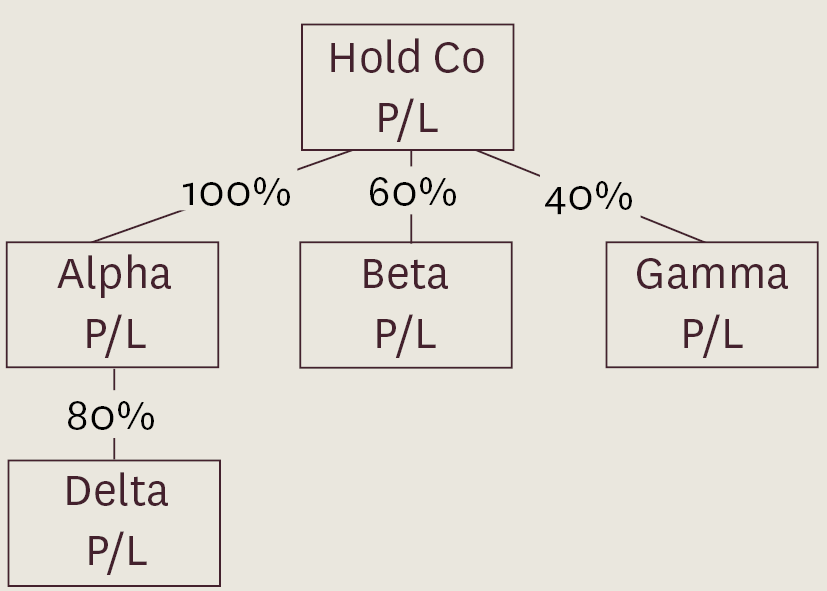

The following is an example of grouping under this test:

Hold Co P/L, Alpha P/L and Beta P/L constitute a group under section 70 of the PTA 2006 as Hold Co P/L holds more than 50% of the issued shares in both Alpha P/L and Beta P/L.

Gamma P/L does not form part of the group as Hold Co P/L holds less than 50% of the issued shares in the company.

Alpha P/L and Delta P/L constitute a group because Alpha P/L holds more than 50% of the issued capital in Delta P/L.

All companies, excluding Gamma P/L, constitute a group because Hold Co P/L is the common ultimate holding company.

A group under test 1 is a mandatory group for payroll tax purposes. As such, the Commissioner cannot de-group such a group. This is discussed in further detail in the next part of our payroll tax series.

Test 2 - shared employees

According to section 71 of the PTA 2007 two or more businesses can also be grouped where they share common employees. Section 71(1) provides:

If one or more employees of an employer perform duties for or in connection with one or more businesses carried on by the employer and one or more other persons, the employer and each of those other persons constitute a group.

While, on the face it, the reach of section 71 appears very wide, its application has been narrowed by the Courts, including in the decision of Commissioner of State Revenue v Liquid Rock Constructions Pty Ltd (2012) VSC 329 (Liquid Rock). In Liquid Rock, Justice Pagone made the following comments at paragraph 7:

The application of s 71 can be difficult because its terms are apt to cover more than the policy of the legislation would suggest. The mere provision of a service to someone by a person employed by another who is otherwise wholly independent, could come within the literal application of the section although that could not be thought to be the purpose, intention or reach of the provision …A person may appear to be performing duties for someone other than the employer when careful analysis will show that not to be the case. It is commonplace for an employee to discharge duties for an employer by provision of duties to another as provision by the employer rather than for or in connection with the business of the other.

Justice Pagone further held at paragraph 8, that for a business to be grouped under section 71 of the Act it is required that the other business to which an employee of an employer is performing duties, must have some practical ability to direct that employee as to the manner of the performance of those duties.

These statements highlight some of the complexity involved in this provision. A review of shared employees must be carefully undertaken to understand whether the arrangements are those intended to be captured by the provision. For example, are there commercial terms underpinning the relationship which would demonstrate an independence of the businesses despite the shared employees? Does the second business have a practical ability to direct the employee?

The answers to these questions may materially affect whether the business should in fact be grouped on the basis of shared employees.

Test 3 - common control

Section 72 of the PTA 2007 deems that one or more businesses will be grouped where a set of persons/entities have a controlling interest in each of two businesses.

These grouping provisions are complex, but, in summary, a controlling interest generally exists where a business is:

conducted by a corporation and a person or set of persons are directors who can exercise more than 50% of the voting power at a director/s meeting or are persons that can influence more than 50% of the voting power of directors or shareholders;

conducted by either an incorporated or unincorporated body and a person or set of persons either constitute more than 50% of the board of management or can control the composition of the board;

conducted by a partnership and a person or set of persons owns (whether beneficially or not) more than 50% of the capital of the partnership or is entitled to more than 50% of the profits of the partnership.

conducted by one person, that person is the sole owner of the business;

in the case of a set of persons, the persons are together, as trustees, the sole owners of the business; or

conducted by the trustee of a trust, that person or set of persons is the beneficiary in respect of more than 50% of the value of the interests in the trust which includes entitlements to profits and capital distributions. In the case of discretionary trusts, a beneficiary has an automatic controlling interest in the trust. This is on the basis that a beneficiary under this type of trust is deemed to have more than 50% of the value of the interests in the trust.

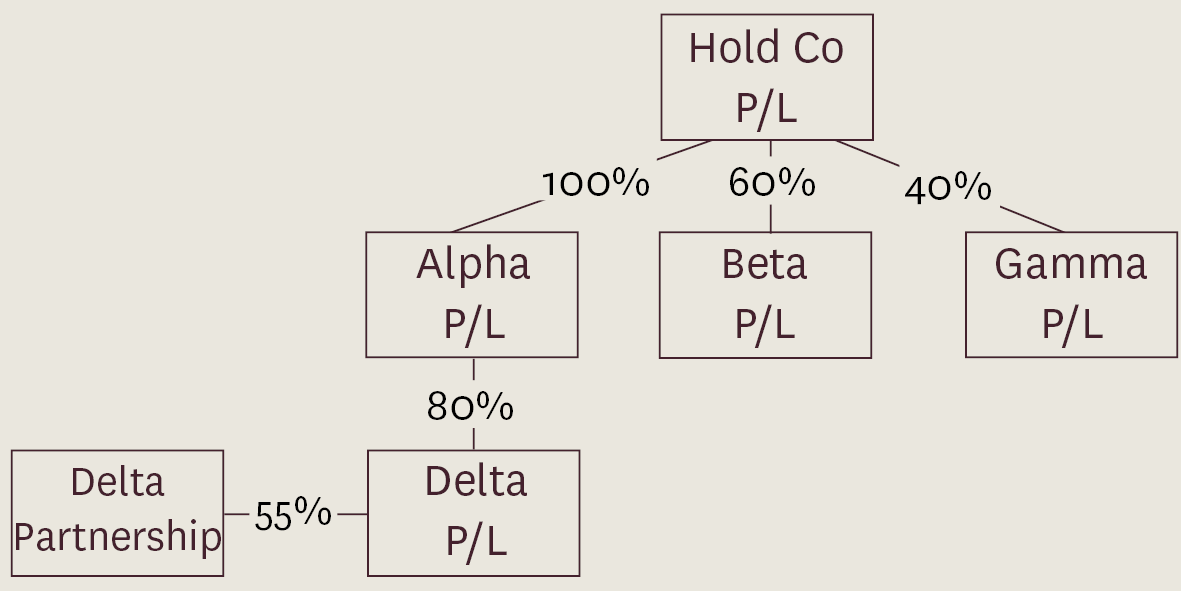

It is important to consider indirect control of companies in addition to direct control. A group may be grouped pursuant to section 50 of the Corps Act (as discussed above) and then additional entities pulled into that group due to a controlling interest.

For example, if we refer to the example above and add an additional fact, being that Delta P/L has a 55% interest in the capital of Delta Partnership, the Hold Co Group (excluding Gamma P/L) will now also include the Delta Partnership as a result of a controlling interest held.

Test 4 - tracing of interests

The tracing provisions are contained in section 73 of the PTA 2007 and provide that an entity will be grouped with a corporation in which the entity has a controlling interest. A controlling interest exists where the entity has a direct interest, an indirect interest or an aggregate interest in the corporation greater than 50%.

A simple example of this is follows:

Epsilon P/L has a 100% direct interest in Zeta P/L and an indirect interest in both Eta P/L and Theta P/L. For the purpose of the grouping provisions Epsilon P/L will only form a group with Zeta P/L and Eta P/L as:

The value of Epsilon P/L’s indirect interest in Eta P/L is 100% x 80% = 80%; however

The value of Epsilon P/L’s indirect interest in Theta P/L is 100% x 80% x 40% = 32%

Epsilon’s indirect interest in Eta exceeds 50%, however its interest in Theta does not and therefore it does not have a controlling interest in Theta P/L when traced.

De-grouping for payroll tax purposes

To avoid anomalies which may arise from the strict application of the grouping provisions, section 79 of the Act provides that an employer that is grouped as a result of common employees, common control, tracing or amalgamation they may apply in writing to the Commissioner of State Revenue to be de-grouped. We discuss this in further detail in the 11th and final instalment of our payroll tax series.

* * *

If you have been grouped for payroll tax purposes and want to understand if this is correct or are concerned that you may be close to breaching the thresholds as a group, contact one of our specialists to discuss the appropriateness of the grouping and options for your business.

Laura Spencer

Senior Associate

M +61 436 436 718 | T +61 3 9611 0110

E lspencer@sladen.com.au

Phil Broderick

Principal

M +61 419 512 801 | T +61 3 9611 0163

E: pbroderick@sladen.com.au

Denise Tan

Senior Associate

M +61 438 714 965 | T +61 3 9611 0160

E: dtan@sladen.com.au