Landholder duty – part 1 – the “basics”

Landholder duty is a regime that was introduced to impose duty on acquisitions in landholding entities. These complicated provisions are difficult to understand, and yet are increasingly becoming a compliance area of focus for revenue authorities. This is Part 1 of a series of articles by our State Taxes Team on landholder duty which deconstructs the complex provisions by providing a snapshot on landholder duty and its application with regards to private entities.

Introduction

Initially, the ‘land-rich’ regime was introduced as an anti-avoidance measure as acquisitions in companies or unit trusts with lands were formerly not subject to duty.

Generally, in order to fall within the old ‘land-rich’ regime an entity not only had to have land holdings with an unencumbered / market value above a certain value (first limb), but also that their land holdings were valued at a certain threshold of the total assets of the entity (second limb).

Over time all States and Territories have now replaced the old ‘land-rich’ regime with the new ‘landholder’ regime, under which now an entity will fall within the landholder duty regime once the first limb is met: if their land holdings are above a minimum value which is set out in each state and territory’s legislation.

When is an entity a landholder?

Across all states and territories, a ‘landholder’ is generally defined to include an entity comprising either a private company or unit trust scheme that has landholdings above a minimum legislated value.

|

|

NSW |

VIC |

QLD |

WA |

|

Type of private entity included as a landholder |

· Private company (includes company limited by guarantee) · Private unit trust |

· Private company · Private unit trust

|

· Private company

|

· Private company (includes company limited by guarantee) · Private unit trust |

|

Section |

s146, Dictionary |

s71 |

s165A |

s155, s152 and s3 |

|

TAS |

ACT |

SA |

NT |

|

Type of private entity included as a landholder |

· Private company (includes company limited by guarantee) · Private unit trust |

· Private company (includes company limited by guarantee) · Private unit trust |

· Private company (includes company limited by guarantee) · Private unit trust |

· Private company (includes company limited by guarantee) · Private unit trust |

|

Section |

s61 and s3 |

s78A and Dictionary |

s91 and s98 |

s4, s56N and s56T |

What are land holdings?

Generally, land holdings are widely defined in all states and territories to include interests in land (including fee simple and leasehold), fixtures or items fixed to land. Some states and territories include in a statutory definition of ‘land’ items such as mining tenements and pipelines.

Lands under uncompleted contracts and completed contracts in relation to landholder entities may also be brought in or out of the deemed land holdings of a landholder.

What is the minimum value?

To fall within the landholder duty regime in each state and territory, an entity (such as a private company or unit trust scheme), must have (direct and indirect) land holdings above a minimum value:

|

|

NSW |

VIC |

QLD |

WA |

|

Minimum value |

For fee simple interest in land – threshold value (registered site value) of $2m or more |

Unencumbered value of $1m or more |

Unencumbered value of $2m or more |

Unencumbered value of $2m or more |

|

Section |

s146 |

s71 |

s165 |

s155 |

|

|

TAS |

ACT |

SA |

NT |

|

Minimum value |

Unencumbered value of $500k or more |

N/A |

N/A |

Unencumbered value of $500k or more |

|

Section |

s61 |

s79 |

s98 |

s56N |

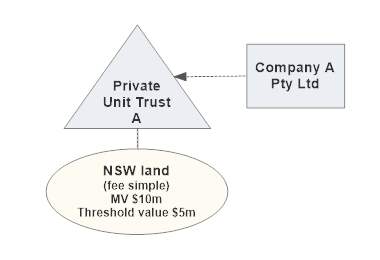

Example – 100% acquisition in private unit trust

To demonstrate practically how landholder duty is applied, in our example below we look as to whether Private Unit Trust A is a landholder under the NSW provisions and if a 100% acquisition in it would trigger duty.

As Private Unit Trust A holds NSW land with a threshold value (registered site value) of over $2m, it is a landholder under the NSW provisions.

Therefore, if Marie acquires 100% of all units in Private Unit Trust A, then Marie would be liable to pay NSW landholder duty of $535,490 calculated as follows:

Dutiable value = 100% x Unencumbered value of land holding ($10m) = $10m

General rate of duty: $40,490 plus $5.50 for every $100 over $1 million

Duty = $40,490 + [($10m - $1m) x 5.5%] = $535,490

In part 2 of this series, we will consider how to identify the landholdings of a landholder.

If you have any further questions on the application of landholder duty or state taxes, please contact one of the members of our specialist team:

Denise Tan

Senior Associate

Sladen Legal

T +61 3 9611 0160 | M +61 438 714 965

Level 5, 707 Collins Street, Melbourne, 3008 Victoria, Australia

E: dtan@sladen.com.au

Laura Spencer

Senior Associate

Sladen Legal

T +61 3 9611 0110

Level 5, 707 Collins Street, Melbourne, 3008, Victoria, Australia

lspencer@sladen.com.au

Phil Broderick

Principal

Sladen Legal

T +61 3 9611 0163 l M +61 419 512 801

Level 5, 707 Collins Street, Melbourne, 3008, Victoria, Australia

E: pbroderick@sladen.com.au

This article refers to sections in each state and territory’s legislation as identified and outlined below:

|

State |

Stamp duty legislation |

|

New South Wales (NSW) |

Duties Act 1997 (NSW) |

|

Victoria (VIC) |

Duties Act 2000 (Vic) |

|

Queensland (QLD) |

Duties Act 2001 (Qld) |

|

Western Australia (WA) |

Duties Act 2008 (WA) |

|

Tasmania (TAS) |

Duties Act 2001 (Tas) |

|

Australian Capital Territory (ACT) |

Duties Act 1999 (ACT) |

|

South Australia (SA) |

Stamp Duties Act 1923 (SA) |

|

Northern Territory (NT) |

Stamp Duty Act (NT) |