Sladen Snippet - Division 7A and Tax Consolidated Groups TD 2015/18

Division 7A of the Income Tax Assessment Act 1936 can operate to deem a dividend to be paid by a private company that is a subsidiary member of an income tax consolidated group (subsidiary).

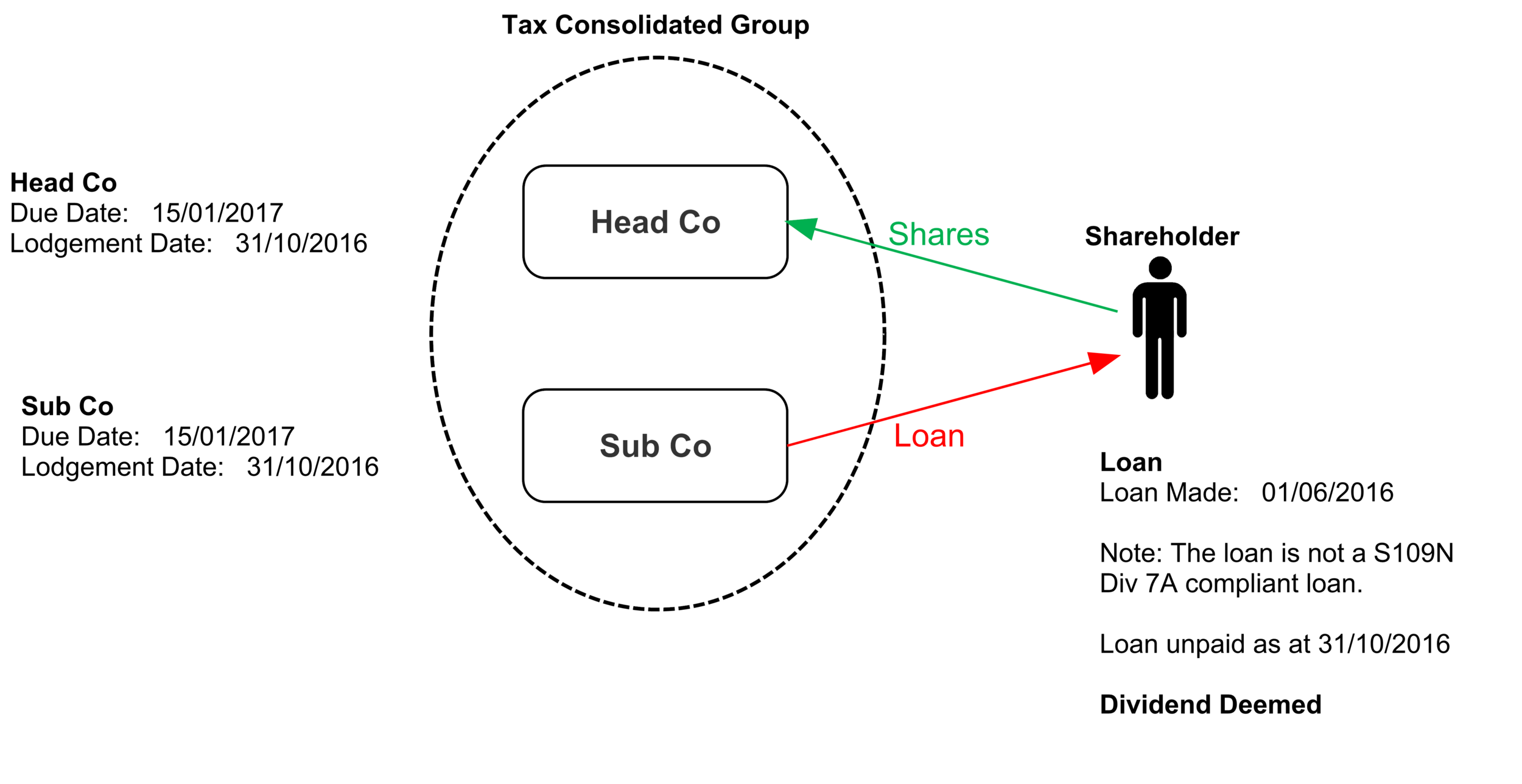

If a subsidiary makes a loan to a shareholder (of the Head Company of the tax consolidated group) or their associate in a manner that evokes the application of the “deemed dividend” provisions in s 109D, the relevant time for complying with the Division 7A provisions would be the “lodgment day” of the Subsidiary’s income tax return for the relevant financial year (s 109D(1)(b)) – however, a Subsidiary member of a tax consolidated group is not required to lodge an income tax return.

The Australian Taxation Office has therefore clarified in Taxation Determination TD 2015/18 that the “lodgment day” for the Subsidiary is taken to be the earlier of the due date for lodgment of the Head Company’s consolidated income tax return for the group for that financial year and the date of lodgement of that return (s 109D(6)). Therefore, Division 7A will be triggered if the loan made by the Subsidiary is not a complying Division 7A loan (for the purposes of s 109N) by that date.

In the example below, a dividend will be deemed to be paid at the end of the 2017 financial year by Sub Co if the loan is not a Division 7A compliant loan and is not repaid by the Head Company by 31 October 2016, being the earlier of the due date (15 January 2017) and lodgement date (31 October 2016).

For further information please contact:

Renuka Somers

Special Counsel

Sladen Legal

M +61 407 478 592| T +61 3 9611 0110

rsomers@sladen.com.au

or

Daniel Smedley

Principal | Accredited Specialist in Tax Law

Sladen Legal

M +61 411 319 327| T +61 3 9611 0105

dsmedley@sladen.com.au