Payday super – exposure draft legislation now open for consultation

As discussed here, the Government previously released a short fact sheet setting out policy design details on the PayDay Super measures scheduled to be effective from 1 July 2026.

The Government has now released exposure draft legislation and explanatory material which is open for consultation until 11 April 2025.

What are the amendments?

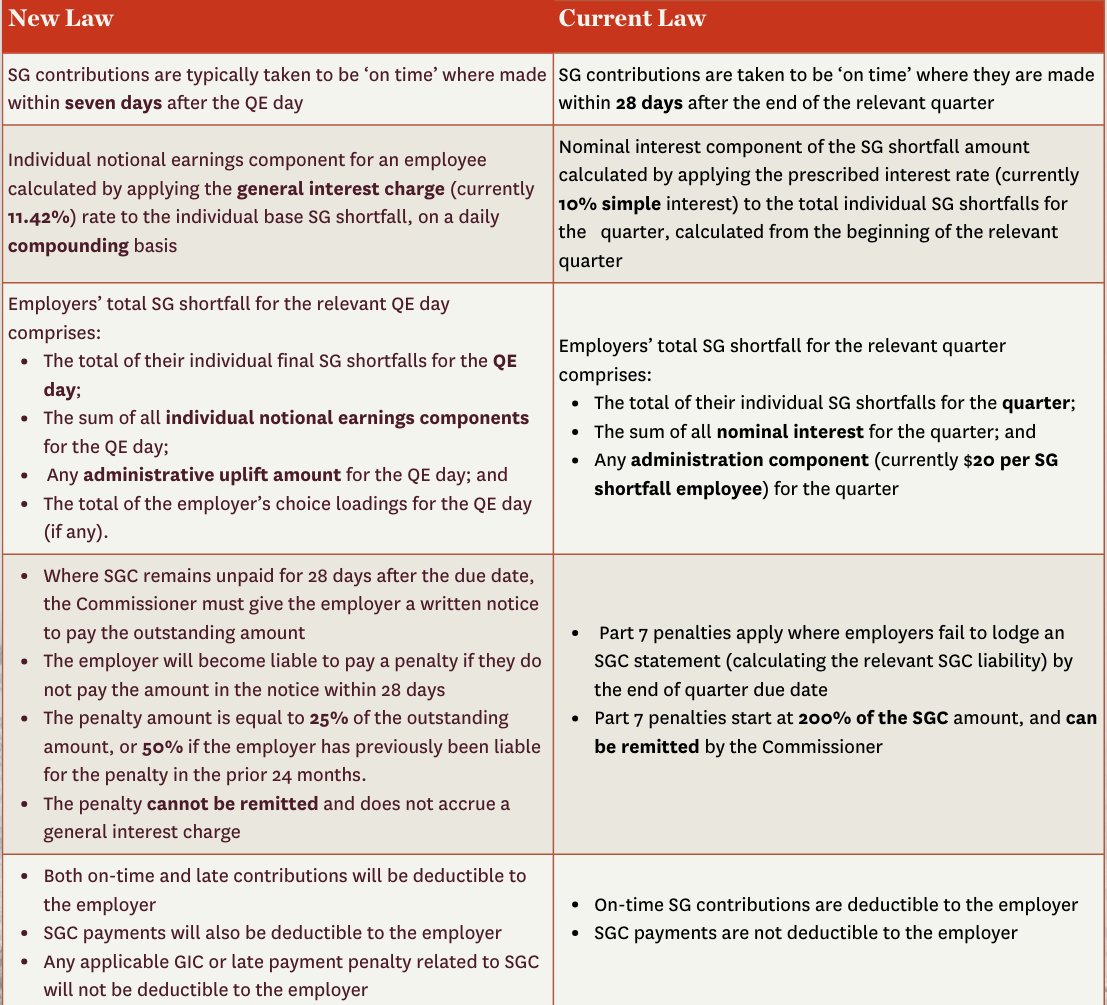

The current super guarantee (SG) regime is legislated as a tax. That is, if an employer fails to make SG contributions on behalf of its employees in the required amount by the deadline for the relevant quarter, it does not ‘contravene’ the super regime. Rather, a tax liability arises as calculated under the super guarantee legislation, known as the SG charge (SGC).

Under current legislative settings, employers are required to make SG contributions at least quarterly. The Payday Super amendments will effectively require employers to align the payment of SG contributions with an employee’s regular pay cycle – for example, weekly, fortnightly, or monthly.

Employers will be compelled to do so via an updated SGC, which is calculated using a new ‘administrative uplift’ component (which replaces the current administration component of $20 per SG shortfall employee).

The policy reasoning behind the new ‘administrative uplift’ component is two-fold:

recognise and recoup the cost to taxpayers of the ATO’s SG enforcement activities; and

incentivise prompt voluntary disclosure to minimise costs to the employer.

The administrative uplift amount will start at 60% of the employer’s SG shortfalls (including notional earnings) but can be reduced where an employer voluntarily discloses late SG payment.

The draft legislation also introduces the new concept of ‘qualifying earnings’ (QE), which are the amount of earnings an employee is paid on which individual SG amounts are calculated. QE are broadly equal to the current concept of ‘ordinary time earnings’, being an employee’s earnings in respect of their ordinary hours of work.

A related new term is ‘QE day’, being the day on which the employer makes a payment of QE to or for the employee.

Other key changes set out under the draft legislation include:

The change to tax deductibility of contributions and the SGC is a welcome and common-sense amendment. This reflects the fact that the SGC is a substitute for payment of super contributions to employees in respect of services rendered, which is itself deductible expenditure for employers.

The Government has invited submissions on the draft legislation, with consultation open until 11 April 2025.

For further information please contact:

Phil Broderick

Principal

T +61 3 9611 0163 l M +61 419 512 801

E pbroderick@sladen.com.au

Philippa Briglia

Special Counsel

T +61 3 9611 0174 | M +61 449 404 801

E: pbriglia@sladen.com.au