Mergers and Acquisitions Reform

2025 will see the biggest changes to Australia’s Mergers and Acquisitions regulatory landscape for a considerable time. On 10 December 2024, the Treasury Laws Amendment (Mergers and Acquisitions Reform) Bill 2024 received Royal Assent resulting in a shift from a voluntary informal review scheme to a mandatory administrative review process. This is a clear statement to focus on protecting competition through merger control.

The reforms introduced by the new legislation aim to preserve competition within markets through the mandatory review of proposed mergers by the Australian Competition and Consumer Commission (ACCC). Such mandatory reviews will be triggered by monetary thresholds based on transaction value and the turnover of transaction participants.

Key changes include:

the requirement for certain transactions of shares, units or assets to be notified to the ACCC for assessment prior to completion of the transaction;

the introduction of a penalty regime to support compliance;

the establishment of a new administrative system where the ACCC will undertake an economic and legal assessment of whether the acquisition is likely to substantially lessen competition in a market, or whether the transaction is of public benefit;

sets clear suspensory timelines for the ACCC to review and decide on notified transactions;

provides for review of ACCC decisions by the Australian Competition Tribunal; and

establishes a public register of notified acquisitions.

When do the changes apply

The reporting obligations will apply to transactions that ‘are put into effect’ (complete/settle) after 1 January 2026 when the changes are slated to commence, however, voluntarily participation may occur after 1 July 2025. This means transactions will be caught under the notification requirements where parties sign transaction documents before 1 January 2026, for example in October 2025, but the transaction is due to complete post 1 January 2026.

This in turn means that deal management and planning for this new process needs to commence now for any transactions expected to complete in the next 6 to 12 months.

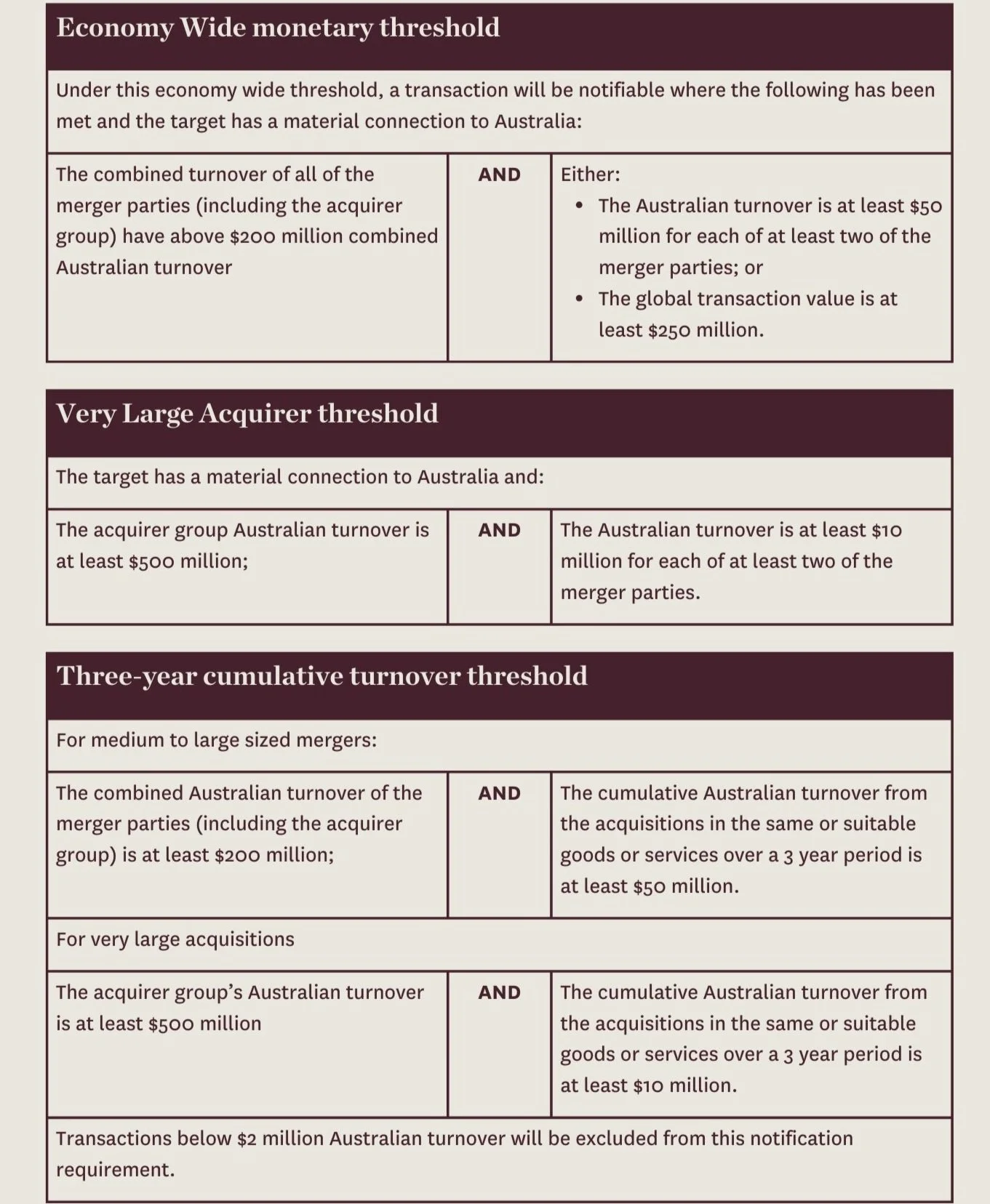

Notification Thresholds

The specific quantum of the notification thresholds will be confirmed in future legislation / regulations and will continually be monitored and updated based on the potential risk to the community over time. However, Treasury have released consultation papers indicating that the thresholds will likely be in line with the following:

A target has a ‘material connection to Australia’ if the target:

is carrying on a business in Australia; or

has plans to carry on a business in Australia.

There remains a number of gaps in the application of these thresholds, including how they are to apply to cross border transactions, how party turnover is to be calculated, how participating entities are to be grouped. Further clarity is expected in future legislature.

Land Exemption

Treasury has flagged an exemption to the notification requirements for transactions which are in respect of;

land acquisition transactions regarding residential land development; or

the business of buying, selling or leasing of property that is not intended to operate as a commercial business.

We await further guidance from Treasury regarding this exemption, particularly in respect of its application to property developers, developing residential land for commercial means.

Specific Scrutiny

Treasury has also indicated the intention to designate specific transactions which from time to time will require notification. Currently such transactions receiving this additional scrutiny include:

transactions involving supermarkets; and

acquisitions meeting the monetary thresholds which include unlisted or private companies acquiring more than 20% of the target.

ACCC Assessment

In assessing proposed transactions, the ACCC will apply the ‘substantial lessening of competition’ test. A proposed transaction may have the effect of substantially lessening competition in a market if

‘it would or would be likely to have the effect of creating, strengthening or entrenching a substantial degree of power in the market’.

A determination of substantially lessening competition will require an assessment of the relevant markets in which the parties to the proposed transaction will operate, whether that is at a national or local level, wholly or partly in Australia.

Assessment Process

Under the changes, the ACCC will take a two phased approach to determining whether the proposed transaction will satisfy the ‘substantial lessening of competition’ test.

Phase 1

All notified transactions will be assessed by the ACCC in an initial stage, where no concerns are raised, the ACCC can issue a determination that the proposed transaction may proceed.

To streamline the review process, Treasury expects that the changes will require this phase 1 process to be completed within 30 business days of notification.

Phase 2

Where the ACCC has concerns that the proposed transaction may substantially lessen competition, the ACCC will commence a more in-depth review stage following written notice to the transacting parties.

This in-depth review stage is expected to be completed within 90 business days of the ACCC’s notification.

If after this Phase 2 has been completed, the ACCC determines that the proposed transaction will substantially lessen competition, the transacting parties may request the ACCC to undertake a public benefit determination. Under this determination the ACCC will decide if the community detriment caused by the lessening of competition will be offset by the community benefit received from the proposed transaction. Such a public benefit determination is expected to occur within a further 50 business days of such a request being made.

The timelines for each of the phases are yet to be legislated and have been put forward by Treasury based on their expectations. At this stage there is inconsistency between the legislations Explanatory Memorandum and Treasury’s released material as to whether the time lines are determined based on business days or calendar days, the result of which could lead to considerable timing differences.

Outcomes

As a result of the ACCC’s review, the ACCC may determine that the proposed transaction:

proceeds without amendment;

proceeds with specific amendments; or

should not proceed.

Consequences of failing to notify the ACCC of a notifiable transaction

A transaction must not be completed where:

the parties are required to notify the ACCC of a transaction based on the notification thresholds, but the transaction has not been so notified;

the ACCC has been notified of the transaction, but the ACCC has not yet made a determination;

the ACCC has determined the transaction must not be put into effect;

an application for a public benefit determination may be made, or has been made but not yet determined;

a person has sought review of the ACCC’s decision through the Australian Competition Tribunal; or

12 months has elapsed after the ACCC made a determination in respect of the notification or public benefit application.

A transaction that has completed or otherwise put into effect where it should not have been, will be rendered void by these changes, civil penalties may also apply.

Fees

As set out in the legislations Explanatory Memorandum, Treasury expects the ACCC’s fees for their review of notifiable transactions to be in the vicinity of $50,000 to $100,000. It is expected that exemptions will apply for transactions involving small businesses. The definition of a small business in this context is yet to be provided.

What do these changes mean for the Australian Merger Market

Parties who will be undertaking transactions in the coming 6 to 12 months should commence planning for their participation in the ACCC review process, this will include:

incorporating a review of the parties turnover considering the proposed notification thresholds in their current due diligence process;

considering the inclusion of condition precedents in respect of the ACCC review in any transaction documents;

undertaking a review of completed transactions from the previous 3 years in light of the proposed 3 year cumulative turn over threshold;

balancing each parties confidentiality and disclosure of information obligations with the information demands of the ACCC review process; and

adjusting transaction timelines and expectations to allow for the ACCC review process.

Please contact any member of our Mergers and Acquisitions team for further insights on the changes covered in this article.

Meagan O’Connor

Principal

T +61 3 9611 0106| M +61 438 531 978

E: moconnor@sladen.com.au

Dean Beaumont

Special Counsel

T +61 3 9611 0129 | M +61 437 257 648

E: dbeaumont@sladen.com.au