A Guide to Understanding Land Tax: Part 3 – Foreign (Absentee Owner) surcharge and the vacant residential land tax surcharge

As discussed in Part 1 and Part 2 of this series, land tax is a state and territory tax levied on the total taxable value of land held by taxpayers in particular jurisdictions. In the case of foreign owners who are deemed to be absent from their properties, additional land tax may be levied on the taxable value of such properties. In Victoria, the foreign person land tax surcharge is known as the absentee owner surcharge regime.

The focus for this series is the Victorian land tax provisions contained in the Land Tax Act 2005 (Vic) (LTA) and for this Part the Victorian absentee owner surcharge. However it is noted that foreign owner surcharges are also apply in New South Wales (2% on all residential land owned by foreign persons), Queensland (2% on all freehold land $350,000 or more owned by foreign persons) and the Australian Capital Territory (0.75% on the average unimproved value of all residential land owned by foreign persons).

What type of land does the absentee surcharge apply to?

In Victoria, the absentee surcharge applies to all classes of land, including residential, commercial, primary production, vacant, etc.

In contrast, in NSW and the ACT, foreign land tax surcharges only apply to residential land.

What is an absentee owner?

From the 2020 land tax year, an absentee owner surcharge of 2% applies to Victorian land owned by an absentee owner. The surcharge rate is in addition to land tax and trust land tax surcharge rates but does not apply to exempt land (discussed in Part 1 of this series).

The definition of ‘absentee owner’ in Victoria is broad and is arguably the broadest definition in Australia. Importantly it differs from and is more far reaching than the definition of ‘foreign purchaser’ used in the stamp duty provisions.

An absentee owner is defined in section 3 of the LTA to mean an absentee person who owns land in Victoria. An absentee person is then defined to mean a natural person absentee, an absentee corporation or an absentee trust. We consider each of these definitions in further detail.

A natural person absentee

A natural person will be an absentee individual where they:

1. are not an Australian citizen or resident; and

2. do not ordinarily reside in Australia, and

3. were either absent from Australia:

3.1. on 31 December of the year prior to the tax year, or

3.2. for more than six months in total in the calendar year prior to the tax year

An ‘Australia citizen or resident’ includes citizens, permanent visa holders and New Zealand citizens who are the holder of a special category visa within the meaning of section 32(1) of the Migration Act 1958 (i.e. are residing in Australia). In the case of permanent residents careful attention should be made to the terms of their visa to ensure it is permanent visa within the meaning of section 30(1) of the Migration Act 1958.

Therefore, in summary, the absentee owner surcharge will apply to natural person landowners as follows:

An Australian citizen and permanent visa holder will never trigger the surcharge, regardless of where they live;

A New Zealand citizen (who is not an Australian citizen or permeant visa holder will not trigger the surcharge if they reside in Australia (at the relevant time);

A person not covered by the two above categories (ie a foreign person) will not trigger the surcharge if they ordinarily reside in Australia, were in Australia on 31 December in the prior land tax year and were in Australia for more than 6 months of the prior land tax year;

A person not covered by the three above categories (ie an absentee natural person) will trigger the surcharge.

An absentee corporation

A corporation will be deemed to be an absentee corporation under the provisions where:

the corporation is incorporated outside Australia; or

an absentee person has an absentee controlling interest in the corporation.

Generally an absentee person will be deemed to have a controlling interest in a corporation where they can control the composition of the board of that company, are able to case more than 50% of the votes cast at a general meeting or hold more than 50% of the issued share capital.

An absentee trust

The definition of an absentee trust first requires an ‘absentee beneficiary’. The definition of absentee beneficiary, akin with ‘absentee person’, includes a natural person absentee, an absentee corporation (except trustees) and the trustee of another absentee trust.

There are then different absentee trust rules for different types of trusts. That is, absentee trust is one in which:

in the case of a fixed trust, at least one of the beneficiaries of the fixed trust is an absentee beneficiary that has a beneficial interest in land the subject of that trust;

in the case of a unit trust, at least one of the unit holders of the unit trust is an absentee beneficiary; or

in the case of a discretionary trust, at least one of the specified beneficiaries of the discretionary trust is an absentee beneficiary.

Determining whether a discretionary trust is an absentee trust

In relation to the discretionary trust test, an analysis must be undertaken as to who a “specified beneficiary” is an absentee. Specified beneficiaries are defined to include beneficiaries who are:

specifically named in the trust deed; or

specifically declared in writing pursuant to the trust deed as a beneficiary.

Therefore, this requires a review as to what beneficiaries are actually named in the trust deed or by a subsequent written declaration. In relation to the former, this will typically include the default beneficiaries (sometimes referred to as the primary or principal beneficiaries). It can also include persons who are not default beneficiaries but are otherwise named as beneficiaries in the trust (sometimes referred to as the additional named beneficiaries).

In relation to the naming requirement, this requires the actual insertion of a beneficiary’s name not merely referencing them by relationship. So, for example, if the default beneficiaries were inserted in the trust deed as “Mary Wu and her children”, Mary Wu would be a specified beneficiary, but her children would not.

The application of this definition means that care that must be taken when choosing who will be the default beneficiary and what other persons are named in the trust deed or who are subsequently declared to be beneficiary. If the absentee surcharge is to be avoided, such persons should not be absentee beneficiaries.

These rules are peculiar to Victoria. For example, in NSW, if any of the discretionary trust’s beneficiaries are foreign persons, then that trust will be a foreign trust for the purposes of the NSW foreign trust surcharge.

Applications that the absentee owner surcharge should not apply

When the absentee owner provisions were introduced into the LTA, sections 3B and 3BA were also introduced. The purpose of these sections is to provide the Victorian Treasurer with the power to determine that the absentee owner surcharge does not apply to certain corporations and trusts. The Treasurer delegates this power to the Commissioner of State Revenue and provided guidelines for the exercise of the power in Victorian Government Gazette No. S 450 dated 1 October 2018.

Effectively, the discretion can be exercised if either the company or trust is not foreign owned or controlled or if the company or trust will make a significant contribution to the Victorian economy and community.

Companies or trusts deemed not be foreign owned or controlled

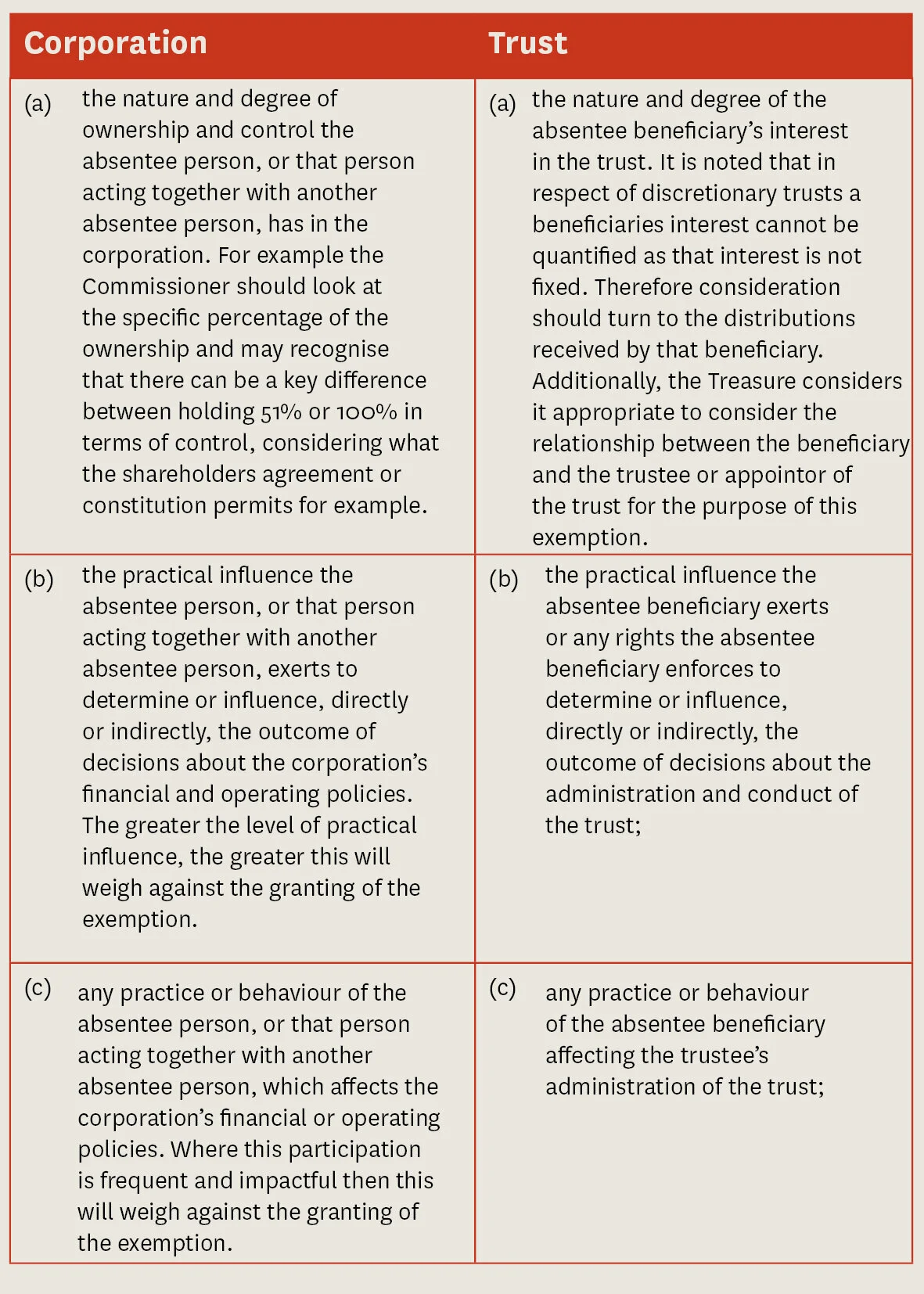

The guidelines require the Commissioner, in exercising his discretion to exempt a party from an absentee owner charge to consider the following:

Foreign companies or trusts that make a significant contribution to the Victorian economy and community

In addition to the above, the Treasurer specifically noted that the absentee corporations or trusts intended to be exempt are:

Australia based companies and trusts;

which make a significant contribution to the Victorian economy and community; and

that exhibit good corporate behaviour.

The above factors are a balance to be considered and all hold different weight. In Kamirice Pty Ltd v Commissioner of State Revenue (Review and Regulation) [2017] VCAT 2087 (14 December 2017) the Commissioner’s decision not to exercise his discretion to exempt an absentee company was upheld by the Tribunal. The taxpayer was a Victorian company, the board of directors of which were entirely Australia, however, ownership was held by a company domiciled in the British Virgin Islands. Senior Member Robert Davis noted at paragraph 110 in relation to the factors:

The weight to be given to each of these matters will depend on the circumstances of each particular case. Having considered all the matters which I have discussed above, I have come to the conclusion that the discretion should not be exercised, so as to exempt Kamirice from the payment of the surcharge. While there are factors that support both sides of the argument, on balance, I have decided that it would be inappropriate in this circumstance to exercise the discretion. In coming to this conclusion, I have taken into account the nature of the investment that Kamirice has made, as well as, the financial input it has had into the community.

What is vacant residential land tax?

In addition to land tax and the absentee owner surcharge, vacant residential land tax applies at a rate of 1% on the capital improved value of vacant residential property in Melbourne’s middle and inner suburbs. The vacant residential land tax potentially applies to all landowners, not just foreign landowners.

To be regarded as vacant the residential property must have, for more than six months in the preceding calendar year, been unoccupied by the owner, a party permitted by the owner to use the property as their principal place of residence or a person under a lease or short term letting arrangement.

Residential property captured by this tax includes homes or apartments and can include land on which a residence is being renovated or constructed. Homes that are exempt from land tax will also be exempt for the purpose of the vacant residential land tax. Additionally, homes that changed ownership, became residential during the year, holiday homes and homes close to workplaces that are separate to the owners PPR may also be exempt.

The vacant residential land tax applies residential properties in the following council areas:

Banyule

Bayside

Boroondara

Darebin

Glen Eira

Hobsons Bay

Manningham

Maribyrnong

Melbourne

Monash

Moonee Valley

Moreland

Port Phillip

Stonnington

Whitehorse

Yarra

Unlike land tax, which is levied against the value of landowner, vacant residential land tax is levied against the capital improved value of the property. That is, it includes the value of the buildings constructed on the land. For properties with valuable buildings and improvements on the land, this can result in significant assessments.

If a property in that location is unoccupied for more than six months during a calendar year, the owner is required to notify the SRO about the property by 15 January of the following year using the SRO’s online portal. For the 2021 land tax year, vacant residential land tax has been waived as part of the Victorian Government's coronavirus relief measures. However, the SRO must still be notified of the vacancy.

If you have any questions about how land tax should apply in your circumstance, please contact our specialist team:

Laura Spencer

Senior Associate

M 0436 436 718 | T +61 3 9611 0110

E: lspencer@sladen.com.au

Thomas Abraham

Senior Associate

M +61 401 387 451 | T +61 3 9611 0178

E tabraham@sladen.com.au

Phil Broderick

Principal

M +61 419 512 801 | T +61 3 9611 0163

E: pbroderick@sladen.com.au