A Guide to Understanding Land Tax: Part 7 - Primary Production Exemption

This is part 7 of our Land Tax Series which aims to deconstruct the various aspects of the complex land tax legislation. To recap: land tax is a state and territory tax levied on the total taxable value of land held by taxpayers in particular jurisdictions. Land tax is assessed on a calendar year basis on the land you own at midnight on 31 December.

In some cases, an exemption may apply to reduce or eliminate your land tax liability. One exemption from land tax is where land is used for primary production. This particular exemption has been highly scrutinised by the revenue authorities in recent years and there has been significant litigation challenging its application. In this article we breakdown the exemption and touch on some key cases which have analysed aspects of the exemption.

As with previous articles our focus will be on the Victorian land tax provisions.

What constitutes primary production for land tax purposes?

Section 64 of the Act defines primary production as:

cultivation for the purpose of selling the produce of cultivation (whether in a natural, processed or converted state); or

the maintenance of animals or poultry for the purpose of selling them or their natural increase or bodily produce; or

the keeping of bees for the purpose of selling their honey; or

commercial fishing, including the preparation for commercial fishing or the storage or preservation of fish or fishing gear; or

the cultivation or propagation for sale of plants seedlings mushrooms or orchids.

‘Purpose’ is a key word in the above definition of primary production. In CDPV Pty Ltd v Commissioner of State Revenue [2017] VSCA 89 (CDPV) the Court of Appeal noted that the question of ‘purpose’ requires consideration of the activities, taking all surrounding circumstances into account including the subjective intention of the person using the land.

In Prestige Land Property Pty Ltd v Commissioner of State Revenue [2021] VCAT 515 the Tribunal also looked at the purpose of primary production activities. The Tribunal held that the activity of ‘chemical fallowing’ was not undertaken for the purpose of cultivating a crop but was done to ascertain whether cultivation was viable on the subject land at all. Therefore, no primary production occurred and the exemption did not apply.

Agistment

Land located outside greater Melbourne, or inside greater Melbourne but not in an urban zone, may qualify for a primary production exemption where it is used for agistment for primary production purpose. That is, provided the owner of the animals normally sells the animals or their offspring then such activities will satisfy the requirement. Agistment of animals for recreational purposes, for example horses for the purposes of riding does not qualify for the exemption. Land within the Melbourne urban zone which is used for agistment will not qualify for the exemption.

What is the primary production land tax exemption?

Sections 65, 66 and 67 of the Land Tax Act 2005 (Vic) (Act) provide land tax exemptions for land used for primary production. The three sections each relate to separate geographical locations:

outside greater Melbourne (section 65);

in greater Melbourne but in in an urban zone (section 66); or

in an urban zone in greater Melbourne (section 67).

The basis for distinguishing these areas is that there are different requirements as to the degree of primary production activities. The extent of primary production activities in each area is as follows:

outside greater Melbourne (section 65) – primarily used for primary production;

in greater Melbourne but in in an urban zone (section 66) – primarily used for primary production; and

in an urban zone in greater Melbourne (section 67) - solely or primarily used for the business of primary production (plus additional requirements, discussed below).

What constitutes land primarily used for primary production?

To be primarily used for primary production for the purpose of section 65 of the Act the area comprising the land must be predominantly used for primary production activities.

In CDPV the Court found that it could not be said that the land was used primarily for cultivation and the selling of the product of such cultivation. At best, the Supreme Court found the activities were a side benefit of holding the property. Croft J identified several important principles in relation to a claim for the primary production exemption under section 66 of the LT Act which can be summarised as follows:

Land will be used ‘primarily’ for primary production if the relevant activities are ‘capable of imparting to the whole parcel of land the necessary character’, with ‘some degree of substance and intensity to them’. By contrast, land will not be used in the required manner if the activities are ‘minimal, slight, spasmodic or token’.

…The scale of activity is not relevant, ‘save and except to show that the relevant cultivation was genuine and not merely colourable’.

It is important to note that supplementary activities such as storing equipment are considered to be part of the primary production activities. However, this must be distinguished from secondary activities which do not constitute primary production. For example, activities of a cattle farmer to process meat on site would be secondary and does not constitute primary production.

In the recent New South Wales case of Chandrala v Chief Commissioner of State Revenue [2021] NSWCATAD 50 (Chandrala) it was determined that the land owned by the applicant had not been used for the dominant purpose of primary production (noting the NSW provisions are similar to the Victorian provisions).

The Tribunal determined that the subjective intention of the landowner will not be enough by itself to satisfy the condition that the land is dominantly used for primary production. It is instead, the ‘current tangible and physical deployment and its purpose’ of the subject land which determines if the land will qualify for the exemption. In Chandrala the landowner’s mere intention to use the land for primary production in the future was insufficient to evidence the land was used for primary production.

What constitutes a business of primary production?

To qualify for the land tax exemption in section 67 the owner of land in an urban zone in greater Melbourne must use the land in a business of primary production. The landowner must be engaged in the business of maintain animals to sell.

To be engaged in a business of primary production the land must be used to conduct one or more primary production activities beyond a recreation or hobby. The business must be viable and be carried out in a business-like manner with a reasonable expectation of profit. The courts have considered whether a business is carried on in various matters. The cases show that there is no predetermined list of factors and each case needs to be considered on its own facts and thus merits.(See for example: Gilbert v FC of T [2010] AATA 882; MR & SL Block & Ors v FC of T [2007] AATA 1897; Kennedy v FC of T [2005] AATA 329; Phippen & Anor v FC of T [2005] AATA 952; Hattrick v FC of T [2008] AATA 301; Peerless Marine PTY LTD v FC of T [2006] AATA 765; Pedley v FC of T [2006] AATA 108.)

Justice Hill in Evans v Federal Commissioner of Taxation (1989) 20 ATR 922 stated that no one indicator could determine whether a business is being carried on, specifying in [939]:

The question of whether a particular activity constitutes a business is often a difficult one involving as it does questions of fact and degree. Although both parties referred me to comments made in decided cases, each of the cases depends upon its own facts and in the ultimate is unhelpful in the resolution of some other and different fact situation.

Objective consideration should therefore be given to each circumstance and reflection as to the availability of evidence to demonstrate the business activities.

In the Supreme Court of Victoria decision of Lotus Oaks Pty Ltd as trustee for the Bozzo Family Trust v Commissioner of State Revenue [2021] VSC 388 (Lotus) the land owner claimed its principal business was primary production on the subject land and that one of its beneficiaries was engaged on a full time basis in that business. However, development operations also undertaken by the landowner were seen to be its principal business.

Justice Garde noted at paragraph 117:

As the legislative history shows, the provisions should be construed relatively strictly – it was not the intention of Parliament to exempt all persons carrying on farming activities from land tax. Rather, the exemption has been progressively narrowed. The practice of ‘land banking’ coupled with minor farming is a particular mischief which the Act seeks to counter.

For a further analysis on the Lotus case see our three part analysis here.

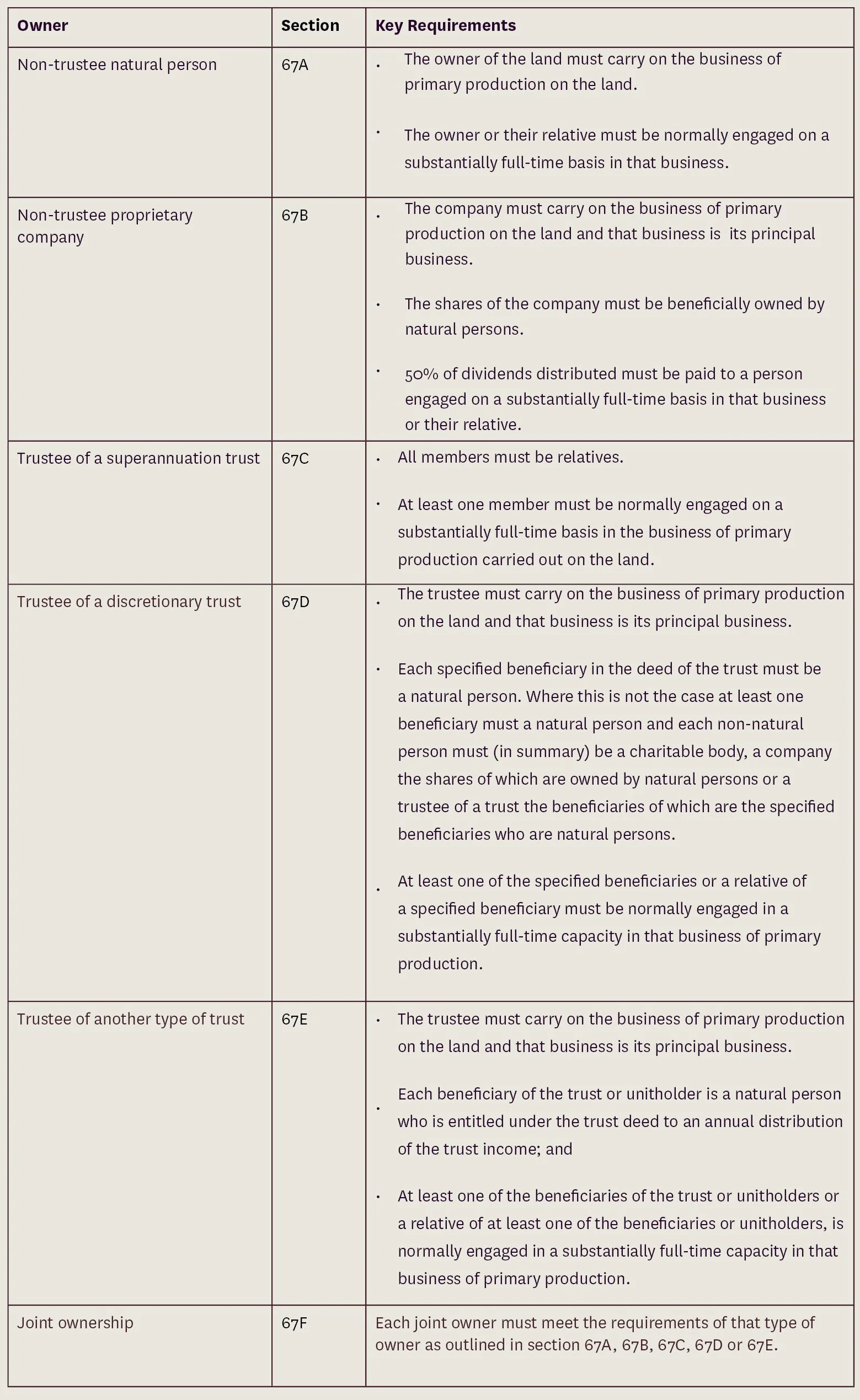

Ownership requirements for the section 67 requirements

Section 67 of the Act was amended in 2019 to include new sections 67A to 67F. These sections include ownership requirements which require there to be a connection between the landholder and the business of primary production undertaken.

The requirements depend on the type of taxpayer. In summary:

These requirements are strict and should be reviewed closely if seeking to apply the exemption in section 67 of the Act.

Preparatory Exemption

Section 68 of the Act provides an exemption where land is being prepared for primary production use, referred to as the ‘preparatory exemption’. To access this exemption an application in writing must be made to the Commissioner of State Revenue (Vic) (Commissioner). The taxpayer must demonstrate that on completion of the activities the land will be exempt from primary production under the exemptions discussed above.

In Revenue Ruling LTA 006, the Commissioner notes that the preparatory activities must be continuous, consistent and unbroken and may include:

clearing of land

establishment of fences

construction of fire breaks

planting of wind breaks

eradication of noxious weeds or vermin

fertilising

ploughing

topsoil enhancement

regeneration of land following salt encroachment; and

establishment of dams or irrigation to ensure adequate water supply

The period between the commencement of the activities and the commencement of the primary production is 12 months. This may be extended to 24 months where the nature and extent of the preparatory work means that the 12-month period would be unreasonable.

The case of Portbury Development Co Pty Ltd as trustee for Portbury Family Trust v Commissioner of State Revenue (Review and Regulation) [2020] VCAT 631 highlights the importance of evidence when seeking an extension of the preparatory exemption. In this case the tribunal ruled that although there is evidence of some work of a remedial or rehabilitative nature being undertaken by the taxpayer on the preparatory work there was insufficient evidence to demonstrate that such activities had the requisite intensity to attract the exemption and have that exemption period extended.

How we can help?

Primary production exemptions for land tax are complex and recent litigation has added further complexity. Our team can help you understand your eligibility to the exemption and assist in applying for the exemption, objecting to a denial of the exemption or responding to SRO audits on point.

For further details contact our specialist team:

Laura Spencer

Senior Associate

M 0436 436 718 | T +61 3 9611 0110

E: lspencer@sladen.com.au

Thomas Abraham

Senior Associate

M +61 401 387 451 | T +61 3 9611 0178

E tabraham@sladen.com.au

Phil Broderick

Principal

M +61 419 512 801 | T +61 3 9611 0163

E: pbroderick@sladen.com.au