Landholder Duty – Part 6 – Acquisition by Control and Anti-Avoidance

Landholder duty is a regime that was introduced to impose duty on acquisitions in landholding entities. These complicated provisions are difficult to understand, and yet are increasingly becoming a compliance area of focus for revenue authorities. This is Part 6 of a series of articles by our State Taxes Team on landholder duty and deconstructs the complex provisions by providing a snapshot on landholder duty and its application with regards to private entities.

In Parts 1 to 5 of our landholder duty article series, we have discussed the different ways landholder duty can arise under the landholder regimes. In this sixth article, we discuss acquisitions via control and anti-avoidance provisions which can deem acquisitions to have occurred. These provisions do not apply in all jurisdictions and therefore can be a trap for advisors and taxpayers. Careful consideration of the far-reaching implications of these provisions should be considered when undertaking transactions.

Control

A unique landholder provision that applies only in Victoria and the Northern Territory is the concept of a relevant acquisition by way of control. The provisions give the Commissioner the discretion to determine that a relevant acquisition has occurred where a person acquires the ability to determine or influence the outcome of the financial and operating decisions or a corporation or unit trust. This influence can be direct or indirect.

In Victoria, section 82 of the Duties Act 2000 (the Act) addresses relevant acquisitions by way of control. It is noted that the provision provides a timeframe for the acquisition of control over three years, meaning that advisors and taxpayers should be mindful when undertaking subsequent transactions.

In determining the application of this rule, consideration is to be given to the practical influence a person may actually have and any practice or behavior which would affect the landholder’s financial or operating policies.

One important aspect is that section 82 applies automatically if there has been an acquisition of control. Not only that but the acquirer of control will be deemed to have acquired 100% of the landholder, unless the Commissioner exercise a discretion to determine a lower percentage interest, including 0%.

Therefore, section 82 must be considered in circumstances such as change in directors, transfer of shares (including shares in a corporate trustee), change of appointors (eg in a unit trust), granting corporate powers of attorney, delegation of board powers etc. One would expect that the Commissioner would not issue an assessment under section 82 for normal commercial dealings in such arrangements, however, it is noted that section 82 would still require an application to the Commissioner (as there is no ability to self assess the Commissioner’s discretion).

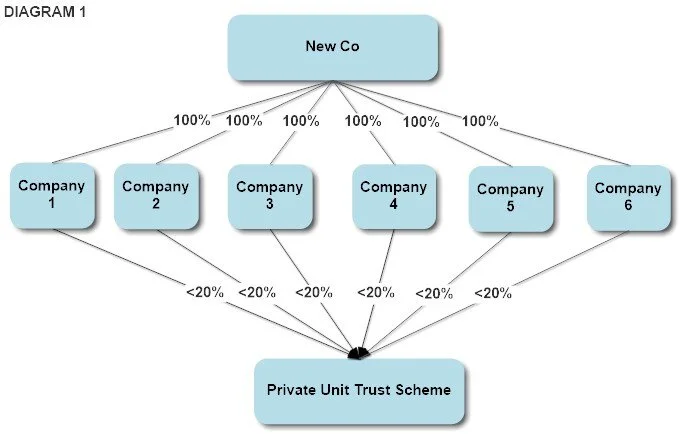

Example

As shown in Diagram 1, a private unit trust, P Trust, is held by 8 companies. Each of the 8 companies owns less than 20% of the company and together they own and control P Unit.

New Co acquires all of the shares in each of the companies. Each acquisition by itself is not a relevant acquisition for landholder purposes as the percentage held by the companies in P Trust is less than 20%.

However, by acquiring all of the shares in all 8 companies, New Co has indirectly gained control over the trust. As such New Co makes a relevant acquisition of 100%.

When undertaking transactions which provide a party control over another interest, advisors and taxpayers should be mindful of the implications of this in light of these rules. In particular, where there is a change of control in a transaction involves the transfer of shares/units that would otherwise be below the relevant acquisition thresholds.

Anti-Avoidance

The landholder provisions were originally introduced as anti-avoidance provisions to address the avoidance of stamp duty as a result of acquisitions into trusts and companies rather than land itself. Nevertheless, general anti-avoidance rules are contained within the legislation of each state and territory to address tax avoidance on an increasingly complex level. Where anti-avoidance provisions apply, the relevant Commissioner is able to reconstruct the transactions as if the schemes had not been undertaken and assess duty accordingly.

There is a notable similarity in the general anti-avoidance provisions in Tasmania, Queensland, Western Australia, New South Wales and the Australian Capital Territory, and the federal anti-avoidance provisions contained in Part IVA of the Income Tax Assessment Act 1936. Specifically, the rules require:

a scheme entered into for the purpose of obtaining a tax benefit;

duty not payable (tax benefit); and

a reconstruction of the transactions which would not result in the tax benefit being obtained.

Whilst ‘scheme’ and benefit are broadly interpreted throughout the various jurisdictions, as they are at a federal level, the ‘purpose’ is assessed differently in each state. Consideration therefore needs to be given to the specific jurisdiction and the factors which that jurisdictions takes into consideration when applying the anti-avoidance rules. For example, in the Australian Capital Territory consideration is given to the extent to which the scheme reduces duty that would otherwise be payable.

In Victoria, the anti-avoidance provisions differ slightly. For example, if the Commissioner considers that a person has participated in a tax avoidance scheme (e.g. an arrangement where an elimination, reduction or postponement of a liability for a person to pay duty occurs), the Commissioner may disregard the scheme and determine and assess for duty that would have been payable but for the scheme.

It is also important to keep in mind that (in particular) the Victorian landholder legislation contains economic entitlement, control and anti-avoidance provisions that are intended to deal with circumstances whereby, without acquiring a significant interest, a person acquires or obtains particular rights within a landholder. As commented by Justice Croft in BPG Caufield Village v Commissioner of State Revenue [2016] VSC 172, these provisions, whilst broad, do not create a separate head of duty.

Advisors and taxpayers must be keenly aware of not only the landholder regimes but also the anti-avoidance rules and should turn their minds to the breath of the legislation when looking at entering to transactions or arrangements involving landholder entities.

If you have any further questions on the application of landholder duty or state taxes, please contact one of the members of our specialist team:

Laura Spencer

Senior Associate

T +61 3 9611 0110

lspencer@sladen.com.au

Denise Tan

Senior Associate

T +61 3 9611 0160 | M +61 438 714 965

E: dtan@sladen.com.au

Phil Broderick

Principal

T +61 3 9611 0163 l M +61 419 512 801

E: pbroderick@sladen.com.au