Corporate Reconstruction and Consolidation Relief from duty – the Victorian provisions and requirements to make an application

Under the Duties Act 2000 (Vic) (Act) there are corporate reconstruction and consolidation relief provisions that provide for an exemption for the direct or indirect transfer of dutiable property (including landholder acquisitions).

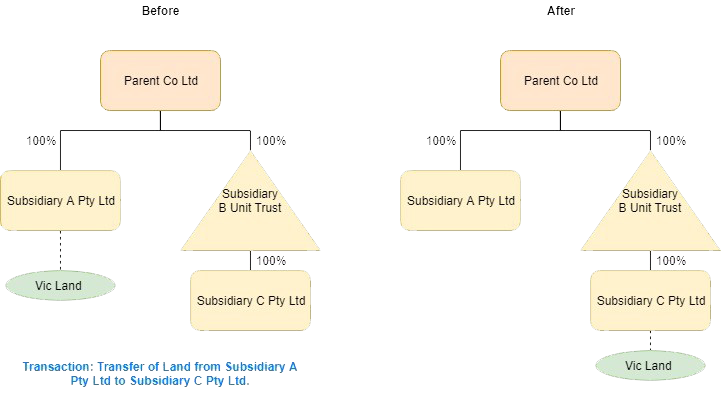

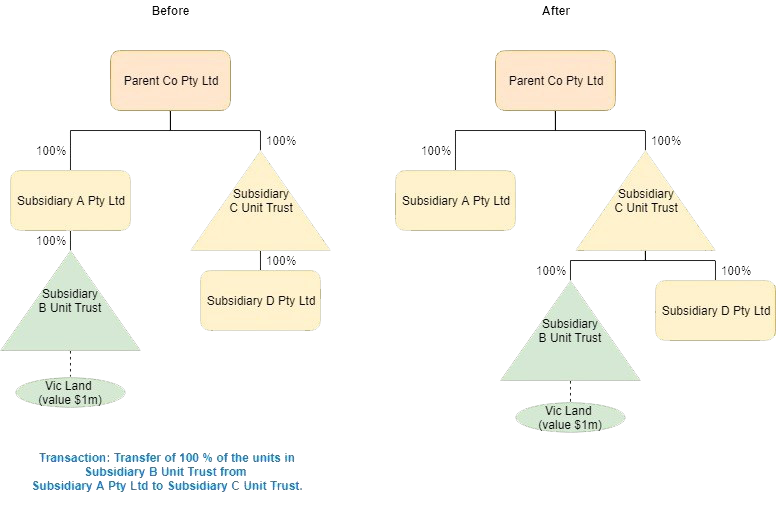

Broadly, the corporate reconstruction relief provisions provide for an exemption of duty to apply where a transfer occurs within members of the same corporate group, which is defined under the Act to mean parent corporations (which includes companies, unit trusts and public offer super funds) and subsidiaries that are at least 90% held.

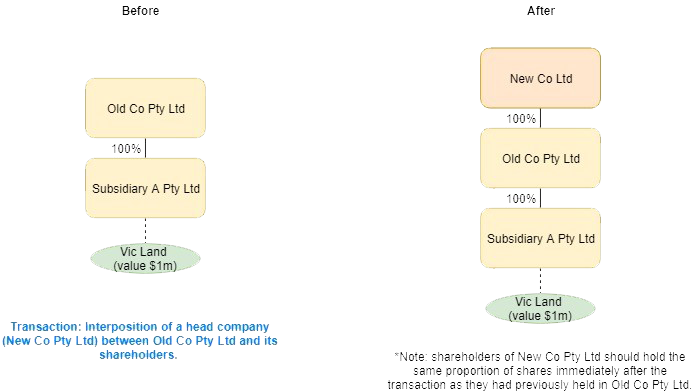

In contrast, the corporate consolidation relief provisions provide for an exemption of duty to apply where a transfer arises in relation to an interposition of a head company between a member of the same corporate group and the shareholders of the member to create a consolidated group for income tax purposes.

The following examples demonstrate the types of transactions that fall within the provisions.

1. Corporate reconstruction relief examples:

2. Corporate consolidation relief example:

We note that there are other complications surrounding the provisions which are not considered here, such as the reasons motivating the transaction/s in question and whether, in relation to a corporate consolidation relief, a consolidated group is required to be formed for income tax purposes.

The provisions contain a requirement under sections 250B(1)(b) and 250DD(1)(b) of the Act which provides that a member of a ‘relevant corporate group’ or ‘consolidated group or consolidatable group’ ‘may apply to the Commissioner for an exemption under this Division [any time before the transaction occurs, or] within 3 years after the [transaction] occurs to which the application relates’.

Recently, investigations have been raised by the Victorian State Revenue Office whereby they have taken the view that sections 250B(1)(b) and 250DD(1)(b) of the Act means that where an application is not made within the 3-year period of the transaction occurring, even if all other requirements of the exemption are met, the transfer of dutiable property or relevant landholder acquisition is subject to duty.

Whilst we disagree with this position, in order to provide clients certainty in their tax affairs, a conservative view of the provisions is recommended and an application for relief should always be made, even where there is a strong position that a relief should otherwise apply.

To discuss this further or for more information please contact:

Denise Tan

Senior Associate

Sladen Legal

T +61 3 9611 0161

Level 5, 707 Collins Street, Melbourne, 3008, Victoria, Australia

E: dtan@sladen.com.au

Phil Broderick

Principal

Sladen Legal

T +61 3 9611 0163 l M +61 419 512 801

Level 5, 707 Collins Street, Melbourne, 3008, Victoria, Australia

E: pbroderick@sladen.com.au