The ATO’s administrative treatment of acquisitions and disposals of interests in ‘no goodwill’ professional practices

This article was written with the assistance of Patricia Martins, Legal Executive / Project Manager.

The ATO has recently released guidelines on its administrative treatment for the application of certain tax issues when interests in ‘no goodwill’ professional partnerships, trusts and incorporated practices (practices) are acquired or disposed.

Broadly, the guidelines apply where:

- the relevant practice qualifies as a “professional practice”, being one that derives income from “the provision of services involving the exercise of specialised knowledge and skill” and where the conduct of its members is regulated by legislation or professional standards of conduct and ethical behaviour administered by a professional body / authority;

- the taxpayer is a practitioner entity that carries on, or participates in the carrying on of, a professional practice as a partner, shareholder, or beneficiary of a trust carrying on that practice (or will satisfy that requirement upon acquiring such an interest);

- the acquisition or disposal of the practice interest occurs on “arm’s length” dealings between unrelated entities during either the admission or exit of a practitioner entity, or a takeover or merger. The “arm’s length” requirement must be demonstrable from the transaction documents and the practice’s governing documents (such as the partnership deed, trust deed, constitution and shareholders’ agreement); and

- the consideration payable or receivable by the practitioner entity has been determined on the basis that the value of goodwill is nil or nominal.

The guidelines do not apply to dealings between related entities, “Everett” type assignments or internal restructures.

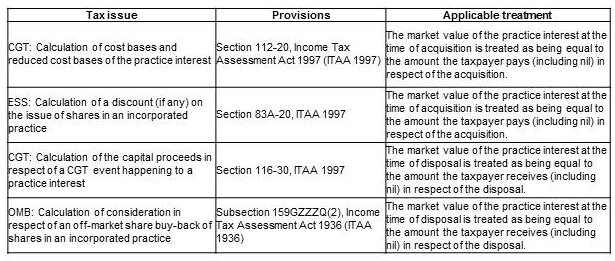

Where these requirements are satisfied, the ATO will not undertake compliance action in relation to the following four tax issues (only) where the taxpayer has adopted the applicable treatment:

These guidelines are intended to operate retrospectively and are more favourable for taxpayers than the guidance formerly contained in the following four ATO publications, which they now replace:

1. Taxation Ruling IT 2540 (paragraphs 13 and 14)

2. Tax Determination TD 2011/26 (now withdrawn)

3. Draft Tax Determination TD 2011/D9 (now withdrawn)

4. Draft Tax Determination TD 2011/D10 (now withdrawn)

These guidelines follow the recent March update of the ATO’s guidelines on Assessing the risk: allocation of profits within professional firms.

To discuss this further or for more information please contact:

Renuka Somers

Special Counsel

Sladen Legal

M +61 407 478 592| T +61 3 9611 0110

rsomers@sladen.com.au

or

Daniel Smedley

Principal | Accredited Specialist in Tax Law

Sladen Legal

M +61 411 319 327| T +61 3 9611 0105

dsmedley@sladen.com.au

or

Patricia Martins

Legal Executive / Project Manager

Sladen Legal

T +61 3 9611 0138

pmartins@sladen.com.au