Sladen Thoughts

Stay up to date with Legal Industry news and updates. Sladen Legal provide regular updates on changes and news in the Australian Legal Industry.

If you are looking for our papers and journal articles including Taxation in Australia, The Tax Institute and SMSF Association, these are available in our Sladen Smart Membership Platform, become a member or login to gain exclusive access.

Author

- Alicia Hill

- Andrea Lin

- Daniel Smedley

- Dean Beaumont

- Edward Skilton

- Edward Hennebry

- Jake Cole

- James Gao

- Jan Harnischmacher

- Jasmine O'Brien

- Jordan Bauer

- Kaitilin Lowdon

- Kseniia Gasiuk

- Magdalena Njokos

- Matthew Davis

- Meagan O'Connor

- Michelle Dowdle

- Neil Brydges

- Nicholas Clifton

- Phil Broderick

- Philippa Briglia

- Sarah Wedd-Elliot

- Sladen Legal

- Sladen Legal

- Thomas Howell

- Victor Di Felice

- Will Monotti

Categories

- Asset Protection

- Business Contracts

- Business Law

- Business Structuring

- Business Succession

- Commercial Contracts

- Commercial Disputes

- Commercialisation

- Conference Papers

- Copyright

- Corporate Advisory

- Cryptocurrency

- Digital Law

- Dispute Resolution

- Employee Share Schemes

- Employment Law

- Entertainment and Sports

- Entrepreneurial

- Estate Disputes

- Estate Litigation

- Family Business

- Federal Taxes

- Franchising

- IP Disputes

- Insolvency

- Intellectual Property

- Inventions

- Land Tax

- Landholder Duty

- Learning

- Managing IP

- Mergers & Acquisitions

- Payroll Tax

- Personal Succession

- Property & Development

- Property Disputes

- Publications

- Sladen Legal News

- Sladen Snippet

- Small Business

- Stamp Duty

- Startups

- State Tax Disputes

- State Taxes

- Superannuation

- Tax Consolidation

- Tax Disputes

- Taxation

- Technology

- Trade Marks

Duty payable on discharge of vendor’s debt by purchaser of land

In the recent decision of Gulliman Pty Ltd v Commissioner of State Revenue [2020] VCAT 804, the Victorian Civil and Administrative Tribunal (Tribunal) held that the discharge of debt owed by vendor to purchaser in respect of previous transaction amounts to non-monetary consideration and, therefore, was subject to land transfer (stamp) duty.

Primary production land exemption denied due to insufficient evidence

Each jurisdiction across Australia has a primary production land tax exemption. The requirements of those exemption are similar.

Court determines payments to a contractor not subject to payroll tax as services found to be ancillary to the supply or use of the goods

Payments made to independent contractors, under “relevant contracts”, are subject to payroll tax under the Payroll Tax Act 2007 (Vic) unless an exemption applies.

Managing Tax and Revenue Office Audits During COVID-19

As the impact of COVID-19 continues to be felt across Australia, federal and state governments continue to take measures to stimulate the economy and provide financial assistance to taxpayers.

Sladen Snippet - VCAT rules land being prepared for primary production and denies exemption from land tax

Most Victorian farmers who are using Victorian land solely or primarily for primary production purposes are aware of the primary production land tax exemptions under section 65, 66 or 67 (Primary Production Land Exemptions) of the Land Tax Act 2005 (the Act).

Sladen Snippet –Trust deeds of discretionary trusts holding NSW residential land must now be amended before 31 December 2020 to avoid foreign surcharges

As referred to in our previous articles, the State Revenue Legislation Further Amendment Bill 2020 (NSW) has now received royal assent on 24 June 2020.

Primary production land tax exemption knocked back – the Annat case

Annat v Commissioner of State Revenue [2020] VSC 108 (Annat) highlights the real risk faced by some farm owners in qualifying for a primary production land tax exemption .

Due to the Victorian State Revenue Office’s approach and scrutiny on primary production lands of late, traditional farming land owners are finding that they now must understand the difficult legislative requirements surrounding primary production land tax exemptions, the resulting structuring and record keeping requirements to ensure that they are not unintentionally exposing themselves to large land tax liabilities.

Sladen snippet: Victorian relief measures in response to the bushfires and COVID-19 pandemic now law

As of 1 May 2020, the State Taxation Acts Amendment (Relief Measures) Act 2020 (Vic) introduces various changes to land transfer duty and payroll tax relief measures as part of the government’s response to provide relief measures for bushfire affected areas and the COVID-19 pandemic.

Sladen Snippet: Additional Tax Relief Announced by the Victorian Government

The Victorian Treasurer Tim Pallas announced on 5 May 2020 that the Victorian Government will provide additional tax relief to businesses suffering as a result of COVID-19. The measures, which bring the Government’s economic survival and job package cost to $1.7billion include:

COVID-19 disruptions on your workforce and how it can shift your payroll tax liabilities to another jurisdiction

The COVID-19 crisis has introduced unprecedented disruptions to the workforce, pushing employees and employers to work in remote capacities and in expedited ways across many industries.

This will mean that employers will soon have to turn their minds to considerations never contemplated before, such as their base line payroll tax assumptions and whether or not changes in the ways we will be working in the coming months, will shift payroll tax liabilities to a different jurisdiction. We explore these questions further in this article.

Transfers to Bare Trusts: Court of Appeal Provides Clarity on Duty Exemption

The Court of Appeal handed down its decision in MD Commercial Pty Ltd v Commissioner of State Revenue [2019] VSCA 295 in late 2019. The decision has provided further clarity on the application of section 35 of the Duties Act 2000 (Vic) which provides an exemption from duty for transfers to bare trusts.

Land tax relief in the midst of the COVID-19 pandemic

State and territory revenue offices continue to make announcements in response to the COVID-19 crisis. Relevant to many taxpayers will be the numerous land tax changes. The changes include rebates, waivers and deferrals for eligible taxpayers.

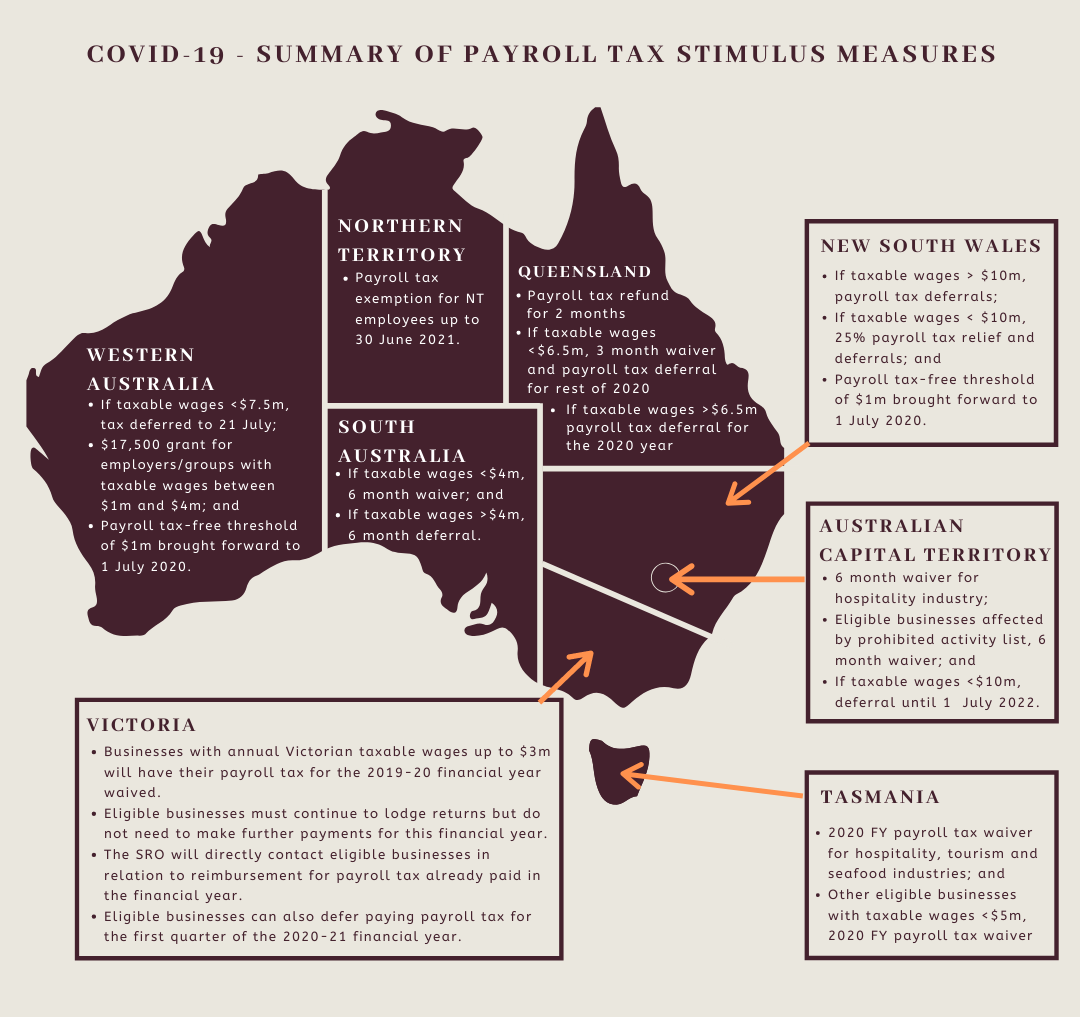

COVID-19 – State and Territory Payroll Tax Stimulus Measures

State and territory revenue offices continue to make announcements in response to the COVID-19 crisis. Relevant to many businesses will be the numerous payroll tax changes. The changes include waivers and deferrals for eligible businesses as well as the bringing forward of cuts to tax-free thresholds in some jurisdictions.

COVID-19: Government and ATO support available

The COVID-19 virus is having a devastating effect on Australian businesses.

Federal, State, and Territory Governments have introduced a range of business stimulus measures and the Australian Taxation Office (ATO) is supplying administrative support to affected taxpayers. We expect further support initiatives as the crisis unfolds.

Sladen snippet - High Court refuses special leave on the Optical Superstore payroll tax case

The clampdown by revenue authorities on investigating medical, dental, optometry and other allied clinics is anticipated to continue, with the High Court refusing to grant special leave to appeal the Victorian Court of Appeal’s decision in the Optical Superstore case.

Sladen snippet – Victorian discretionary trust deeds must be amended by 1 March 2020 to avoid foreign duty surcharge

The State Revenue Office (SRO) have announced that its current “practical approach” in relation to whether trustees of discretionary trusts trigger the foreign duty surcharge will cease from 1 March 2020.

Sladen Snippet - It’s not too late for your NSW discretionary trust holding residential land

As outlined in our previous article, the State Revenue Further Amendment Bill 2019 (NSW) was introduced to NSW Legislative Assembly on Tuesday 22 October 2019, and proposed to make changes to New South Wales land tax and duty legislation.

Sladen snippet – does your discretionary trust hold residential land in NSW? If so, you may need to amend its deed by 31 December 2019

As outlined in our previous article, under the proposed changes to New South Wales land tax and duty legislation, a trustee of a discretionary trust (including testamentary trusts) will be deemed to be a “foreign trust” if the terms of the trust do not prevent a foreign person from being a beneficiary of the discretionary trust. Importantly, these changes are proposed to have retrospective effect to the 2017, 2018 and 2019 land tax years and can catch dutiable transactions back to 21 June 2016.

Sladen Snippet – NSW Discretionary Trusts to be Deemed Foreign Trusts Under Proposed Legislation

The State Revenue Legislation Further Amendment Bill 2019 was introduced to NSW Legislative Assembly on Tuesday 22 October 2019.

Sladen Snippet - Access to the primary production land tax exemption to be further restricted for Melbourne farms

Primary producers in Melbourne will soon be faced with a greater likelihood of paying land tax on their farms due to the proposed reform, and narrowing, of the primary production land tax exemption as proposed in the State Taxation Acts Further Amendment Bill 2019.