Payroll Tax Series – Part 5 – Victorian concessional regional rates

In part 5 of our payroll tax series, we outline how employers may qualify for concessional Victorian regional payroll tax rates.

Thousands of businesses across regional Victoria have already taken advantage of the Victorian Government’s regional payroll tax cuts, which have saved businesses more than $31 million in the first financial year it was introduced.

The regional payroll tax rates are:

2019 and 2020 financial years: 2.425%

2021 financial year: 2.02%

2022 financial year: 1.62%

2023 financial year onwards: 1.2125%

Due COVID-19 relief measures announced, a reduced rate of 1.2125% will apply from 1 July 2019 to regional employers in bushfire affected areas.

Which employers are eligible to receive the regional payroll tax rate?

Regional employers who are based in regional Victoria (First requirement) and pay at least 85% of Victorian taxable wages to regional employees (Second requirement) will qualify for the regional payroll tax rate.

First requirement: Based in regional Victoria

An employer is based in regional Victoria if it either has an ABN and a registered business address regional Victoria or if it does not have an ABN has its principal place of business in regional Victoria.

In general, this is determined with reference to the state of affairs in the month the wages were paid. Where businesses move addresses during a month, the location of an employer will be determined with reference to the state of affairs on the last day of the month.

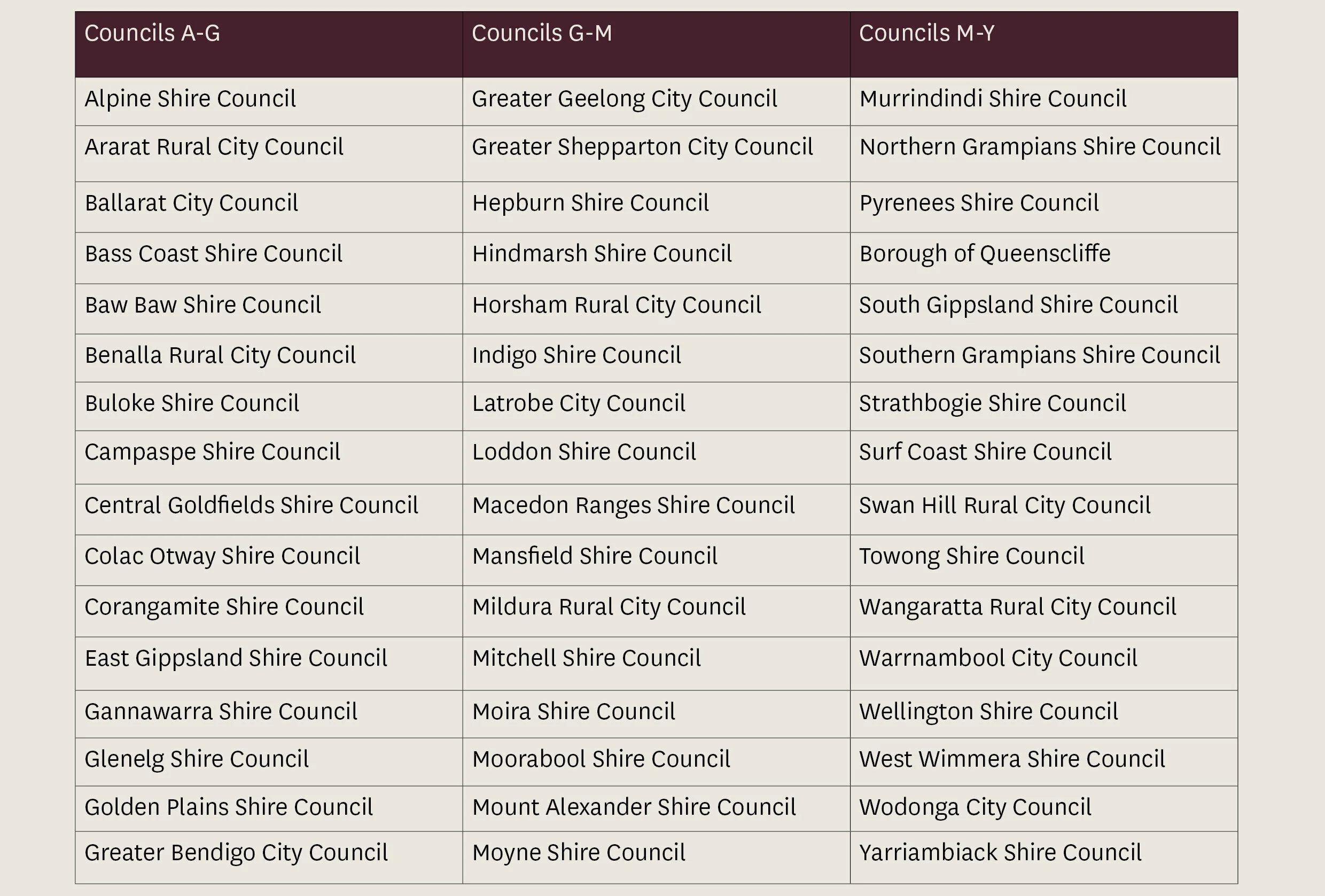

Regional Victoria is defined to include a certain regional councils. The qualifying regional councils are listed in the table below.

Second requirement: 85% of wages paid to regional employees

To qualify for the regional payroll tax rate, a regional employer must also pay at least 85% of its monthly Victorian taxable wages to regional employees under both the monthly payroll tax returns and the annual payroll tax return.

A regional employee is an employee who performs services for their regional employer mainly in regional Victoria in a month. Whilst there is no legislative guidance on what ‘mainly’ means, the State Revenue Office indicates this would be satisfied where more than 50% of an employee’s services is performed in regional Victoria during a month.

Restructuring your business

Any business that has a Victorian regional presence but is below the 85% threshold could consider a restructure to ensure the regional part of their business is eligible to access the discounted regional payroll tax rate.

Any restructure must be carefully considered and implemented. Not only should anti-avoidance provisions be considered but other issues that could arise out of such a restructure. These could include:

Triggering tax or duty by moving to the new structure;

Employment law issues of moving employees to a new structure;

Assignments of leases and other documents required in such a restructure;

The need to put in place new internal processes and intra group dealings.

If you have any questions about how payroll tax should apply in your circumstance, please contact our specialist team at:

Denise Tan

Senior Associate

T +61 3 9611 0160 | M +61 438 714 965

E: dtan@sladen.com.au

Laura Spencer

Senior Associate

T +61 3 9611 0110

lspencer@sladen.com.au

Phil Broderick

Principal

T +61 3 9611 0163 l M +61 419 512 801

E: pbroderick@sladen.com.au