A Guide To Understanding Land Tax: Part 1 Overview of Land Tax

Part 1: Overview of Land Tax

What is land tax

Land tax is a state and territory tax. It is an annual tax that is levied by the state authorities of each state and territory based on the total taxable value of land held in the particular jurisdiction.

In general, an entity is liable for land tax where the total taxable value of all the land owned in a particular state or territory, excluding exempt land, exceeds a threshold value.

When an entity’s taxable value of all land owned in the particular state or territory exceeds the threshold, land tax is levied at the applicable rates.

Typically, a land tax assessment is issued by the relevant authorities formalising the land tax liability.

This land tax series will mainly focus on the state of Victoria, and the applicable land tax provisions pertaining to Victoria.

Current legislation and revenue authority

The Land Tax Act 2005 (Vic) (LTA) is the current legislation that governs land tax in Victoria.

The LTA is administered by the State Revenue Office of Victoria.

Imposition of land tax and liability

Land tax is imposed annually on all taxable land in Victoria. An owner of taxable land is liable to pay land tax on the land.

Examples of taxable land are:

Investment properties

Holiday homes

Vacant land

Commercial properties

Land tax is not levied on exempt land. Examples of the types of exempt land are:

Principal place of residence

Primary production land

Land leased for sporting, recreational or cultural activities by members of the public

Land owned or used by charitable institutions

Health centres and services

Rooming houses

Retirement villages

Caravan parks

Crown land

The most common exemptions will be discussed in further detail in the upcoming parts of this series. More particularly, the principal place of residence exemption, the primary production exemptions and charities and other exemptions.

Who is an owner of land?

At first instance, it may seem straightforward what or who an owner of land is.

However, the definition of “owner” under the LTA is broad and includes any of the following persons:

a person entitled to land for a freehold estate in possession;

a person entitled to land under a licence of Crown land if the person has a right, absolute or conditional, of acquiring the fee simple;

a person who is a licensee of vested land under Part 3A of the Victorian Plantations Corporation Act 1993;

The most common definition of “owner” above is a person who is entitled to land for a freehold estate in possession. In simple terms, a person who has purchased land and is registered on the land’s certificate of title.

It should be noted that there is no particular requirement for the type of entity that can be an owner of land. An owner of land can therefore be an individual, company or the trustee of a trust.

Joint owners

If you own land with others, you are considered to be a joint owner of land.

Under the LTA, joint owners of land are to be jointly assessed for land tax on the land as if it were owned by a single person.

In so doing, each jointly owned land is assessed as an individual joint ownership, with an assessment issued to the joint owner.

A land tax assessment issued to each joint ownership is made without regard to the separate interests of each joint owner or any other land owned by any joint owner (either alone or jointly with someone else).

A joint owner that owns land individually is also then issued a separate individual land tax assessment on all the taxable lands they own in any capacity.

These two stages are summarised below:

Stage 1 - Joint ownership assessment

Joint owners assessed together and one of the owners is issued a joint ownership assessment on behalf of all the joint owners. All the joint owners are liable for the land tax together.Stage 2 - Individual assessment

Each joint owner is assessed individually on all the taxable lands they own in any capacity, including their proportional interest in any jointly owned land.

A joint ownership deduction applies under the individual assessment, being the lesser of:

The particular joint owner’s share of the tax in the joint ownership assessment; or

The amount of tax calculated in the individual assessment representing the individual’s share in the jointly owned land.

The joint ownership deduction is explained in further detail on the SRO’s website.

Assessment of land tax

If a land tax liability exists, a taxpayer is assessed for land tax on the total taxable value of all taxable land of which the taxpayer was the owner at midnight on 31 December immediately preceding that tax year.

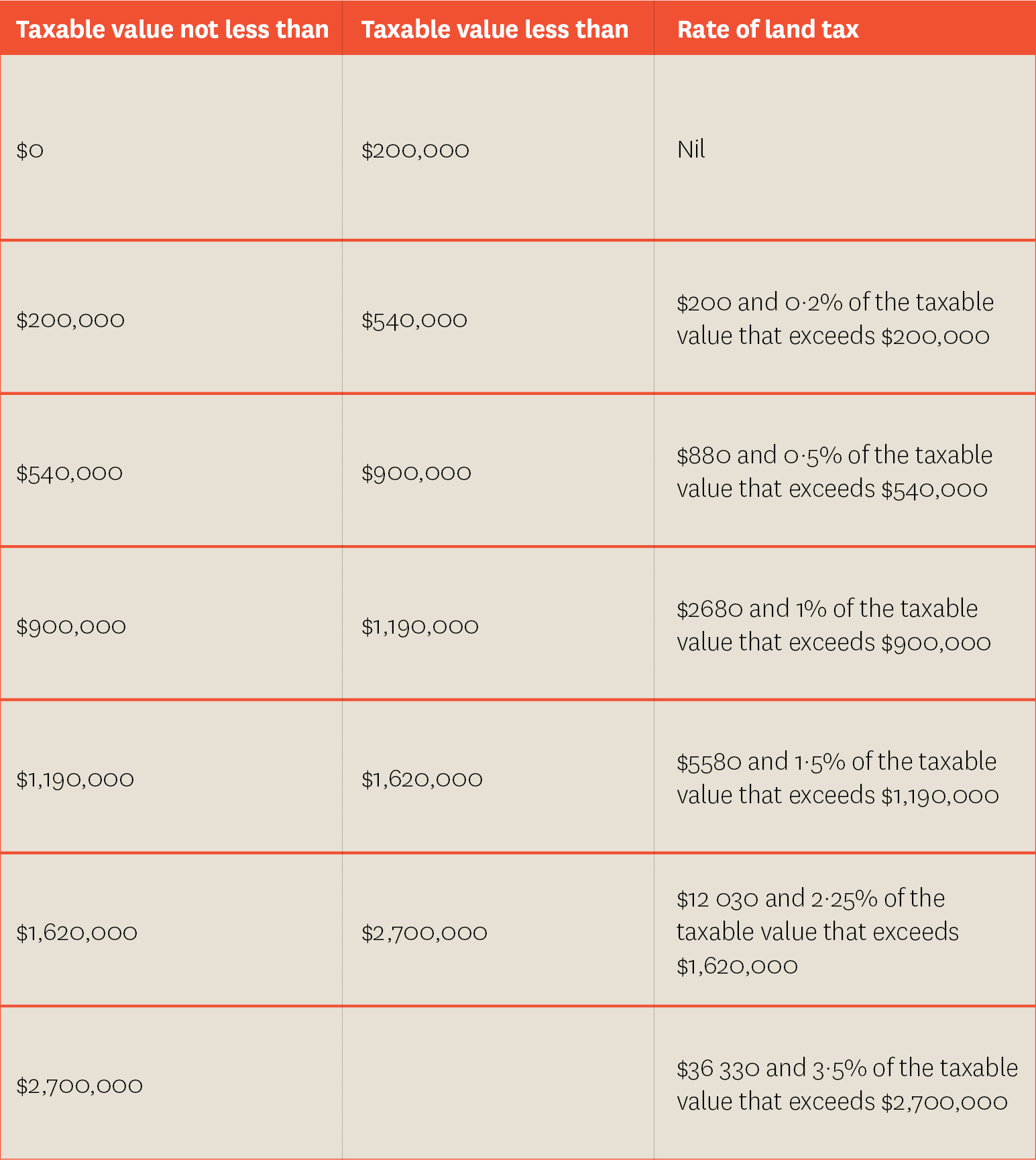

The rate of land tax (general rate) is as follows:

Land tax assessments are generally issued to the taxpayer or the taxpayer’s authorised representative between January and late May each year.

However, if land tax exemptions were incorrectly applied for particular lands in previous years, land tax assessments may be issued outside the general timeframe.

Questions

If you have any questions about how land tax should apply in your circumstance, please contact our specialist team:

Phil Broderick

Principal

M +61 419 512 801 | T +61 3 9611 0163

E: pbroderick@sladen.com.au

Laura Spencer

Senior Associate

M 0436 436 718 | T +61 3 9611 0110

E: lspencer@sladen.com.au

Thomas Abraham

Senior Associate

M +61 401 387 451 | T +61 3 9611 0178

E tabraham@sladen.com.au